Web Articles New lease accounting standard

2025/10/20

Complete Explanation] New Lease Accounting Standards Effective in 2027|Outline, Changes, Impact, and Practical Responses

The new lease accounting standard effective from April 2027 is a major revision that, in principle, requires many contracts that were previously treated as off-balance sheet to be recorded on the balance sheet. As a result, the scope of work to be undertaken by accountants will be broader than ever before, including inventorying of contracts, lease judgments, discount calculations, review of journal entries and notes, and system support.

This article will provide a comprehensive explanation of the following

Background of the new standard and timing of application

・ Differences from the current system and major changes

・ Impact on financial statements and management indices

・ Practical considerations and impact by industry

・ Preparation steps for application and system support

At the end of each chapter, we summarize [main points of this chapter]. Those who want to grasp the whole picture can go through the chapters in order, and those who want to know only the necessary parts can efficiently review the chapters starting from the main points. We hope that this article will help you to understand how you should prepare for the new lease accounting standards and organize the overall picture of your response.

Table of Contents

1. overview and background of the new lease accounting standard【differences from IFRS 16

The new lease accounting standard (ASBJ Statement No.34 and ASBJ Guidance No.33) is, A system in which a lessee in principle accounts for leases on-balance sheet and recognizes a "right-of-use asset" and a "lease liability" on the balance sheet. The objective is to increase transparency of financial information. The objective is to increase transparency of financial information and ensure international comparability.

Under the previous system, there were cases where lease liabilities were not represented in the financial statements depending on the type of contract. In particular, contracts that have been treated as operating leases have not been able to sufficiently show future cash outflows, making it difficult for investors and financial institutions to grasp the actual status of the company.

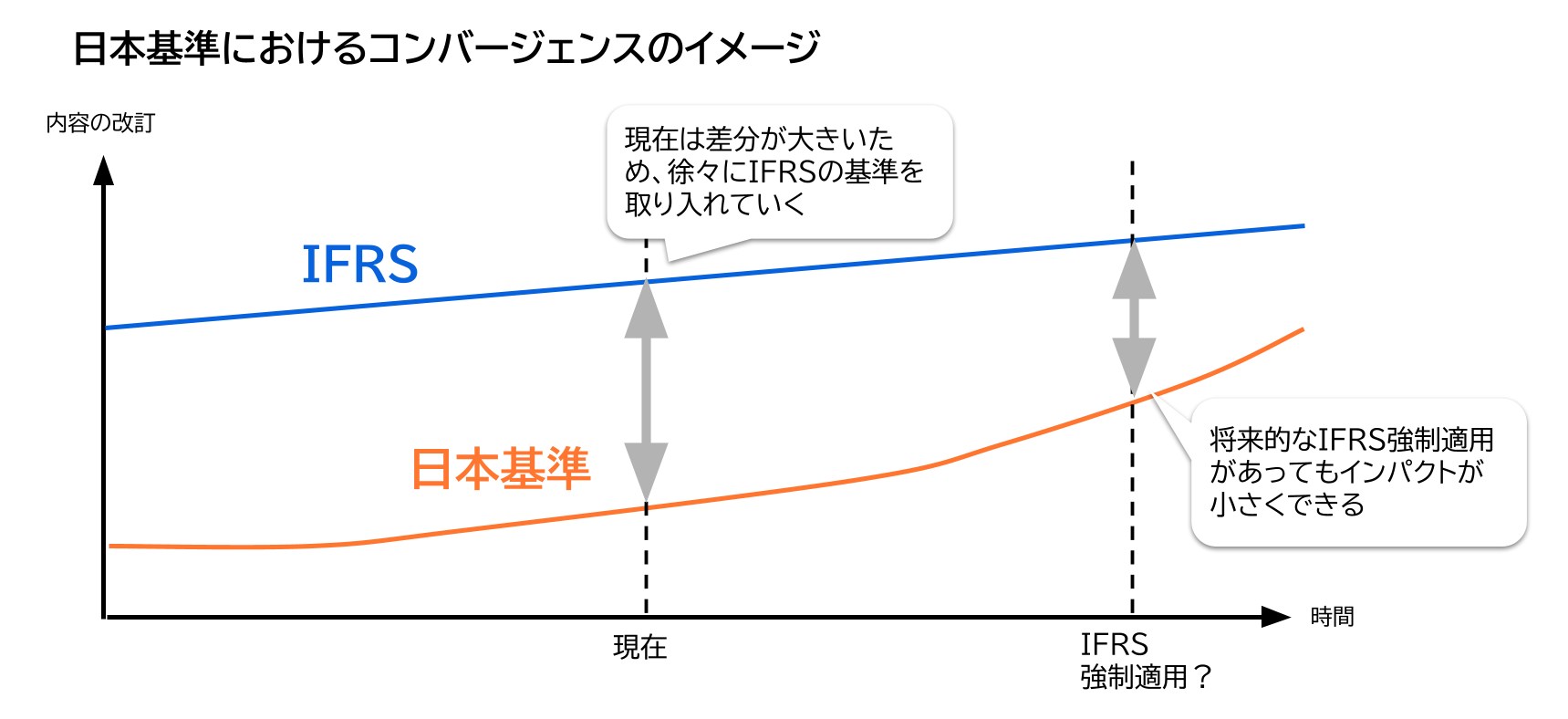

The background behind the development of the "New Lease Accounting Standard" is as follows, IFRS (International Financial Reporting Standards) The background to the development of the "New Lease Accounting Standard" is a move to ensure comparability with IFRS (International Financial Reporting Standards). In Japan, since the 2000s, in order to facilitate comparisons with foreign companies Since the 2000s, Japan has been pursuing a policy of "changing its accounting standards to those similar to IFRS This policy has been promoted in Japan since the 2000s to facilitate comparison with foreign companies. With regard to lease accounting, IFRS 16, which was effective from the fiscal year ending March 31, 2020 onward, thoroughly implements on-balance sheet treatment, and the gap between IFRS 16 and Japanese GAAP has been widening. With the objective of narrowing this gap, a new lease accounting standard has been issued in Japan.

As described above, the new lease accounting standard will be While ensuring comparability with international standards, the new lease accounting standards The new lease accounting standard aims to realize more realistic financial reporting by clarifying assets and liabilities associated with the use of leases, which were not easily represented in financial statements in the past.

Key Points of this Chapter

- The new lease accounting standard will, in principle, treat leases on-balance and record right-of-use assets and lease liabilities.

- The objective is to improve transparency of financial information and ensure international comparability.

- Under the previous system, lease liabilities were not easily represented in financial statements, which was a challenge.

- It was introduced to reduce the difference with IFRS 16.

The outline of the system, changes, and timing of application are organized in a compact manner. It is ideal for those who want to understand the entire picture of the new lease accounting standard in a short time.

2. effective date of the new lease accounting standard and target companies [effective April 2027

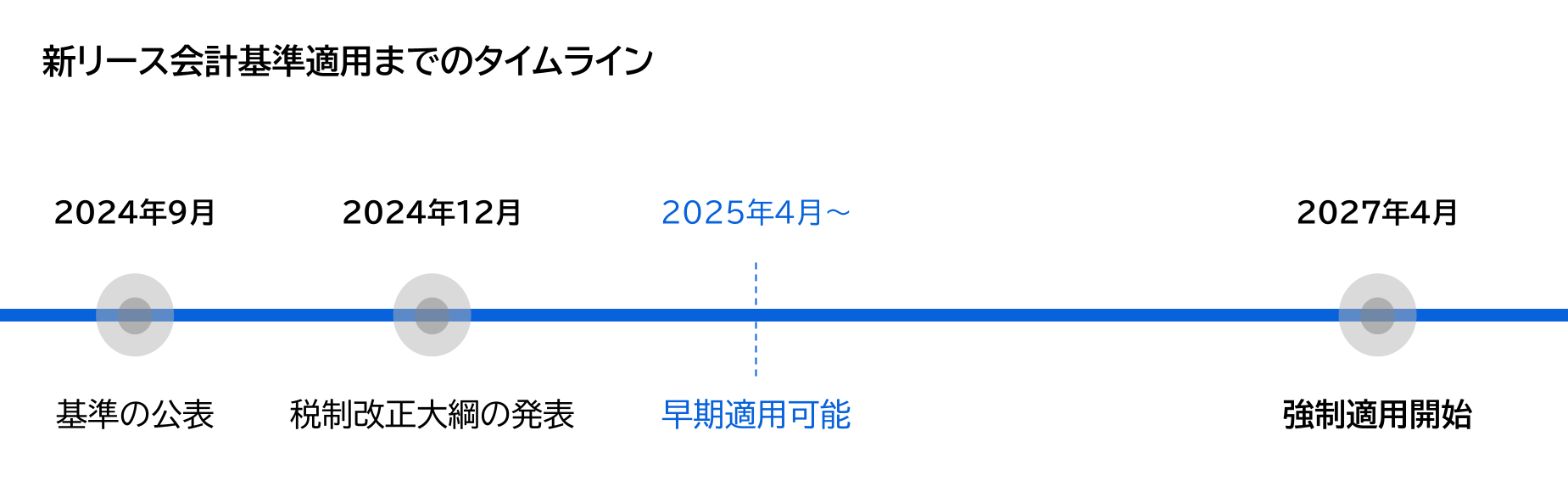

The new lease accounting standard was issued by the Accounting Standards Board of Japan (ASBJ) on September 13, 2024. Mandatory application is from the beginning of fiscal years beginning on or after April 1, 2027. Although it will be Early application for fiscal years beginning on or after April 1, 2025 also be possible to do so. Until mandatory adoption begins, the existing standard will continue to be used. On the other hand, an entity that chooses early adoption will be required to account for leases in accordance with the new lease accounting standard.

Furthermore, in December 2024, the Tax Reform Proposal was released, which partially revised the taxation system related to lease accounting. As changes are underway in both accounting standards and the taxation system, companies are required to estimate the degree of impact on their accounting practices and to grasp the scope of their preparations as early as possible.

Companies subject to the application

- Listed companies and their affiliates (subsidiaries and affiliated companies)

- Company with accounting auditor

- Large companies under the Companies Act and their subsidiaries (capital of 500 million yen or more or total liabilities of 20 billion yen or more)

These companies will be required to apply the new lease accounting standards and must be prepared.

Treatment of small and medium-sized enterprises

For small and medium-sized enterprises, the application of the new lease accounting standard is voluntary unless they fall under the above-mentioned "enterprises subject to the application". Although it is not mandatory, If the parent company is listed on a stock exchange or if transparency of financial information is required by business partners may be required to take action. For example, as a member of a consolidated group, it may be necessary to conform to the policy of the parent company, or it may be necessary to adjust the content of disclosures in negotiations with financial institutions.

What is required for application

For the application of the new lease accounting standard, the impact of the system change is not limited to financial statements, business processes, internal controls, group development, disclosure systems, system development, and even the tax reporting process. The new lease accounting standard will affect not only financial statements but also business processes, internal controls, group development, disclosure systems, systems development, and even tax reporting processes. Based on the timing and scope of application, it is necessary to consider early on whether your company will be included in the scope and when you should start preparing.

Key Points of this Chapter

- Publication is scheduled for September 2024, and mandatory application is scheduled for April 2027 (early application is possible after 2025).

- The impact will be widespread in both accounting and taxation.

- The scope includes listed companies, subsidiaries, companies with auditors, and large companies.

- Small and medium-sized companies apply on a voluntary basis, but may be required to comply at the request of their parent company or business partners.

- There is a limited period of time before the application, and preparation including contract management and system maintenance is required.

Differences from the Current Standard and Major Changes (including Exceptions and Transitional Measures)

The following is a summary of the differences between the existing standard and the new lease accounting standard.

3.1 Basic differences between old and new

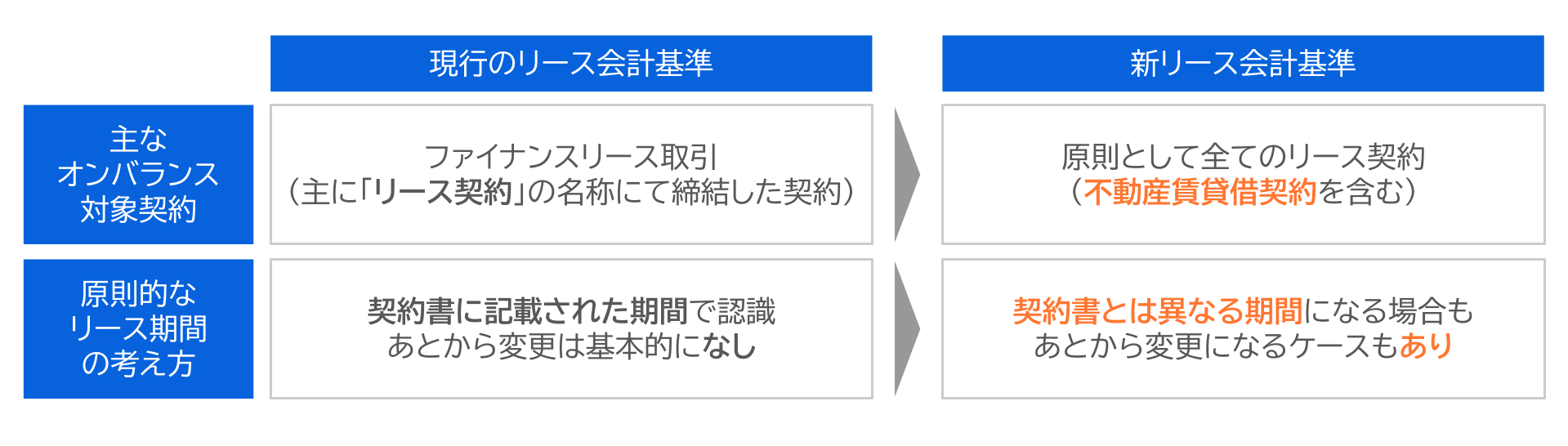

The new lease accounting standard significantly changes the accounting treatment of leases for lessees. In particular, The differences from the current standard are clear in terms of the scope of leases to be on-balance sheet, the accounting items, the method of expensing, and the contents of notes The new lease accounting standard is clearly different from the current standard in terms of the scope of leases to be

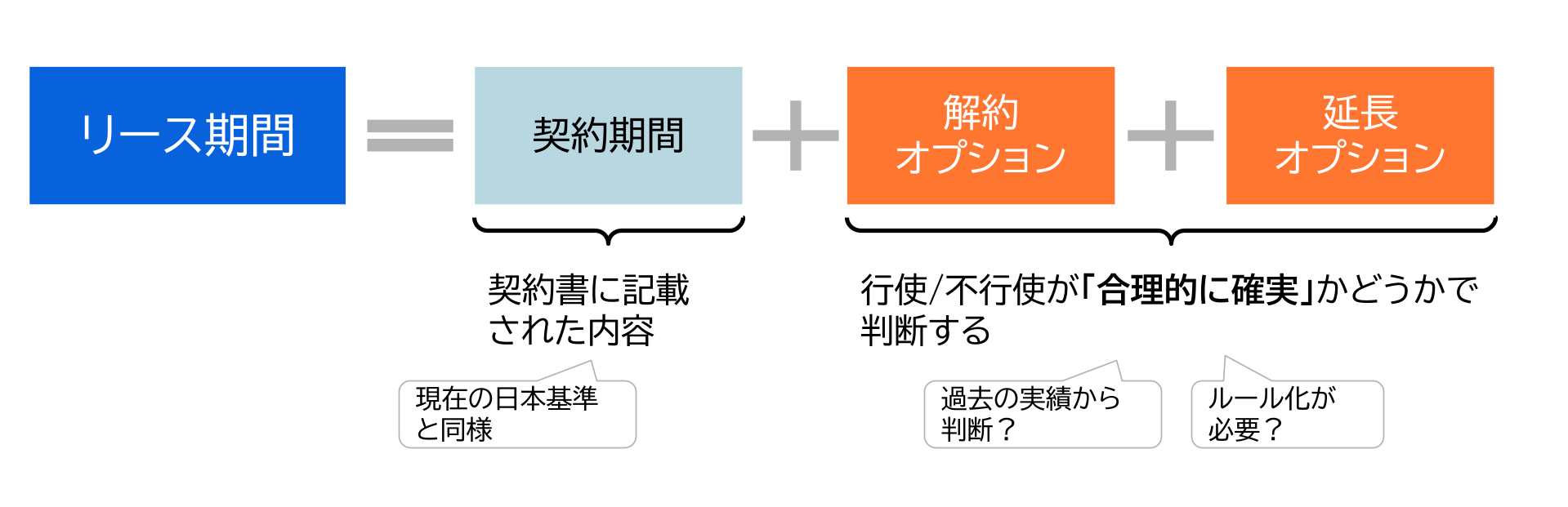

In addition, the new lease accounting standard also changes the The new lease accounting standard also includes a significant change in the method of estimating the lease term.The new lease accounting standard also includes a significant change in the method of estimating the lease term. In the past, the lease term was generally based on the term specified in the contract, but under the new standard, in addition, thelesseeis required toreasonably estimate the possibility of exercising options to extend or terminate the lease.

For example, in a real estate lease contract, even if the contract is for a short term, the more reasonably certain it is that the lessee will actually renew and continue to use the property, the more likely it is that the lessee will be required to include that term in the lease term. Conversely, if it is reasonably certain that the lease will be terminated early, the lease term could be shorter than the term stated in the contract.

Thus, the lease term is not only a contractual provision, The new standard is characterized by the need to estimate the lease term based not only on the terms of the contract, but also on factors such as economic incentives that may influence the decision to extend or terminate the contract. This is a feature of the new standard.

The new standard is characterized by the need to estimate the lease term based not only on the terms of the contract, but also on the factors that provide economic incentives to the lessee to extend or terminate the contract. A Survey of Major Companies

3.2 Exceptions (including the concept of materiality)

Under the new lease accounting standard, in principle, all lease transactions are treated as on-balance sheet transactions, but exceptional treatments are permitted if certain conditions are met. Typical examples are as follows.

- Short-term leases

Lease term 12 months or less (excluding those with purchase options) A lessor can choose off-balance sheet treatment for a contract with a lease term of 12 months or less (excluding a contract with a purchase option). - Small leases

Based on internal materiality criteria, assets with small amounts (e.g., operations up to a total value of around 3 million yen) may be expensed as incurred. (e.g., operations up to a total amount of approximately 3 million yen) can choose to be expensed. - Simplified treatment

If the materiality is low, a simplified method such as the gross amount method or the straight-line interest method can be adopted.

For immaterial transactions, a simplified treatment may be applied to reduce the burden. In making such a judgment, the concept of using the relative size to total assets as one guideline is helpful. For example, if the balance of future minimum lease payments is generally less than 10% of the total of the amount of such outstanding lease payments and the balance of fixed assets, there is room to consider using the simplified treatment.

3.3 Transitional measures (at the time of transition)

The new lease accounting standard includes a transitional provision that specifies how to treat existing contracts at the time of initial application (transition date). Since it would be practically burdensome to treat all contracts retrospectively to the new standard on the first day of application, the new standard allows a method that allows transition based on the carrying amount of existing contracts and the residual lease payments. This is intended to reduce the transition burden on companies while maintaining financial statement continuity.

- Old finance lease

A lessee is allowed to take over the book value of leased assets and lease obligations at the end of the previous period as the book value at the beginning of the new lease accounting standard. -

Former operating lease (Choose either one)

・ The discounted present value of the remaining lease payments at the beginning of the period is recognized as a lease liability, and the same amount is recognized as a right-of-use asset in principle

・The method A lessee calculates the right-of-use asset if it is applied from the inception of the contract, and adjusts the difference by retained earnings. - Choice of short-term or small amount

An entity can choose to account for leases off-balance sheet even after the transition. However, the reason and scope of the selection should be decided in advance. policy in advance. The policy should be made in advance to ensure the stability of the operation.

Which method should be adopted for former operating leases? Should the priority be placed on smooth transition with less burden on the lessee, or should the priority be placed on the precision and comparability of the financial figures? The new lease accounting standard requires a decision to be made based on the following perspectives.

Summary of Major Changes

-

Contracts subject to on-balance sheet

The contracts to be recorded on the balance sheet (B/S) are not limited to those clearly marked as "lease contracts". In principle, all transactions that are determined to be leases as a matter of fact are covered, including real estate lease contracts. Therefore, retailers that lease a large number of stores and companies that own a large number of leased company housing are likely to be significantly affected. - Concept of lease term

Not only the term stated in the contract, The lease term should be estimated taking into account the possibility of extending the lease term or exercising termination options. The lease term should be estimated taking into account the possibility of extending the lease term or exercising termination options. For example, in a real estate lease contract, the term should take into account the possibility of contract renewal. As a result, there may be cases where a longer lease term than before is used, which may affect the amount of right-of-use assets and lease liabilities recognized.

Key Points of this Chapter

- In principle, lease transactions will be treated as on-balance sheet transactions, and the scope will be expanded.

- The term should be estimated taking into account extension and cancellation options.

- Exceptions and transitional measures are provided for short-term and small value leases.

- Real estate lease contracts will also be subject to this rule, which will have a significant impact on industries.

4. journal entries and tax treatment under the new lease accounting standard (lessee-side accounting, subleases, and tax discrepancies)

In this section, we will summarize the accounting procedures for lessees based on the new lease accounting standards. In addition to the processing flow and journal entry examples, we will also review sublease transactions and discrepancies with taxation, which are likely to cause issues in practice.

4.1 Accounting Flow (Lessee)

Under the new lease accounting standard, a lessee is required to account for leases in the following manner

1. Identification of leases

Contracts. Is the right to control the use of the identified asset transferred is determined by the substance of the contract. Even if the name of the contract is "rental" or "lease," if the contract is recognized as a lease in substance, it is subject to the lease.

2. classification of leases/services

Separate out ancillary services that are included in the lease payments, such as human services for systems associated with the leased property. The extent to which a lease is treated as a lease is an important decision point for accounting purposes.

Determination of lease term

Non-cancelable term In addition to, extension and cancellation options The lease term is the period of the non-cancelability of the lease. In some cases, the term of the lease may be different from the term stated in the contract, and especially for real estate contracts, the possibility of renewal should be taken into account in the estimation.

4. Initial recognition

Calculate the present value of future lease payments The present value of the lease payments to be made in the future is calculated The present value of the lease payments to be made in the future is calculated and a lease liability is recognized. In principle, the same amount should be recognized as a right-of-use asset, but there may be cases in which adjustments for incidental expenses or lease incentives are necessary.

5. Subsequent measurement

A right-of-use asset is depreciated over the useful life or lease term. Depreciation and the lease liability is depreciated based on the useful life and lease term. In principle, interest expense is recognized based on the interest method. The right-of-use asset is depreciated based on its useful life and lease term. This is different from the conventional straight line treatment of lease payments in that the expense is allocated between "depreciation expense" and "interest expense".

4.2 Basic form of journal entries (lessee)

Under the new lease accounting standard, a right-of-use asset and a lease liability are recognized on the balance sheet, and then reflected in the income statement as depreciation expense and interest expense. The basic journal entries are as follows

At inception

(Debt) Right-of-use asset / (Credit) Lease liability

At the time of each term payment

(Lease liabilities / (Credit) Cash and deposits

(B) Interest expense

(Depreciation expense / Accumulated depreciation

The actual payment is divided into the repayment portion of the lease liability and the interest portion, and the right-of-use asset is depreciated over the useful life or lease term.

Due to this treatment, The balance sheet shows the asset and the liability, and the income statement shows depreciation and interest expense. The income statement shows depreciation and interest expense. This is a significant change from the conventional operating lease in which the lease payments are recorded as a lump-sum expense.

*The details of the journalization pattern and specific accounting procedures are also introduced in a related article.

What journalizations and accounting procedures are required under IFRS 16 (New Lease Accounting Standard)?

Particularly in the initial years, total expenses tend to be higher due to the impact of interest expense, and income statement figures are more likely to fluctuate compared to the previous straight-line lease accounting treatment. As a result, while operating income and EBITDA levels appear higher than before, net income is affected in some cases.

4.3 Image when subleasing is involved

Under the new lease accounting standard, sublease contracts will be recognized as finance leases in many cases. The reason for this is that what was previously determined based on the "underlying asset" is now replaced by the "right-of-use asset," making it easier to qualify for full payout recognition.

In this case, accounting procedures occur for both the lessee and the lessor, and journal entries become more complex. A typical flow chart is shown below.

At the inception of the head lease

(Debt) Right-of-use asset / (Credit) Lease liability

At the beginning of sublease (Recognition by lessor)

(Debt)/(Credit) right-of-use asset

(Debits) Accumulated depreciation / (Credits) Profit (or difference adjustment)

At the time of receipt of sublease income

(B) Cash and cash equivalents / (C) Investment in leased assets

(Borrowing) Interest income

At the time of payment of head lease

(Lease liabilities / (Credit) Cash and deposits

(B) Interest expense

Thus, in a sublease recognition of the extinguishment of the right-of-use asset and the addition of a journal entry for profit and loss and additional journal entries for profit and loss are required, making accounting treatment more complicated than in the past.

In addition, the following issues arise in practice.

- Finance Lease Determination Based on Reconciliation of Lessee's and Lessor's Information

- Extinguishment of the right-of-use asset and recognition of gain or loss at the inception of the sublease

- Calculation and journal entry of interest income

- Treatment of reinstatement of the right-of-use asset at the occurrence of termination

The risk of errors is high when these are done manually, Therefore, automation and strengthening of internal control are required in many cases by using a system that can manage lessees and lessors in an integrated manner. Lease accounting

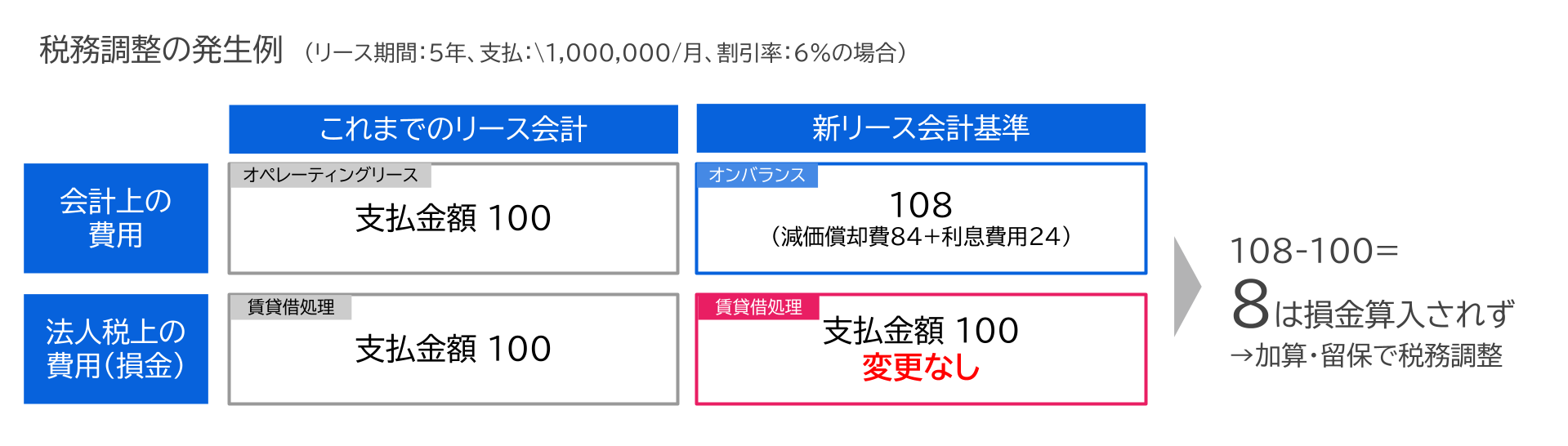

4.4 Discrepancies with Taxation (Tax Association Discrepancies)

Under the new lease accounting standards, there will be many cases where there is a difference between accounting treatment and tax treatment. For accounting purposes, "depreciation of the right-of-use asset and interest expense on the lease liability." for accounting purposes. On the other hand, for tax purposes, the accounting treatment is the same as before. "the amount of payment (debt settled basis)" as before. The difference between the two amounts is therefore Therefore, there is a difference between the two amounts. This causes a "tax discrepancy" For example, a lease term of 5 years and a certain lease payment of 1.5 million yen are

Specific examples

For example, assuming a lease term of 5 years, a fixed lease payment of 1,000,000 yen per month, and a discount rate of 6%, depreciation expense + interest expense = 108 for accounting purposes, while the actual payment is treated as 100 for tax purposes. This difference is Subject to declaration adjustment (addition or retention) The difference is subject to adjustment (addition or withholding). Since this difference varies depending on the nature of the contract and the discount rate, an appropriate management system is required.

Practical Issues

- The need to simultaneously manage different amounts for accounting and tax purposes.

- A deductible schedule must be prepared and the treatment of differences must be tracked from year to year.

- Tax reporting adjustments are required.

In addition, since operating leases are on-balance sheet for accounting purposes, there will be a tax discrepancy in the former operating leases that are on-balance sheet.

Practical issues to be addressed

- Establishment of a double ledger

Establish a system to maintain accounting and tax amounts at the same time. - Management of loss recognition schedule

Record the accrual of differences by fiscal year and clarify the retention and elimination of differences. - Tax return reconciliation

Summarize the basis for differences in a form that can be explained externally. -

System Support

Introduce a system with full payout determination, retention of the amount for tax purposes, and output function for tax reporting.

Having these in place in advance will facilitate procedures in closing and reporting and reduce risks in audits and tax audits.

Key Points of this Chapter

- Lessees will record lease liabilities and right-of-use assets, and expenses will be divided into depreciation and interest expense.

- Sublease journal entries will become more complex and require system management.

- Taxes are based on the amount paid, resulting in tax discrepancies and requiring ledgers and documentation.

5. impact on financial statements, business indicators, and disclosures (including sale and leaseback)

The new lease accounting standards will have a broad impact on the three financial tables and key management indicators. Unlike traditional off-balance sheet accounting, assets and liabilities will be recorded on the balance sheet, changing the financial picture itself.

Impact on Balance Sheet (B/S)

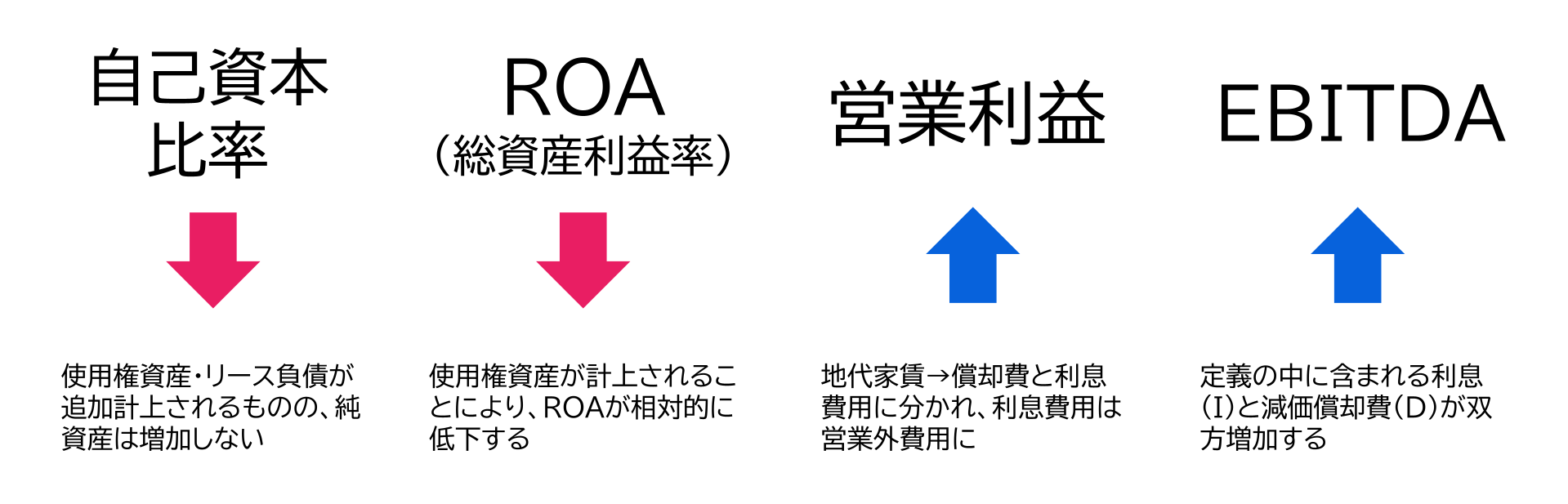

by the new recognition of right-of-use assets and lease liabilities, Total assets and total liabilities will both increase Total assets and total liabilities will both increase. Especially for companies with many long-term real estate leases and large equipment leases, the increase in liabilities will be large, which may result in a decrease in the equity ratio. As a result, the capital adequacy ratio may decline. This could result in a decline in the capital adequacy ratio.

Impact on Profit and Loss Statement (P/L)

Under the new lease accounting standard, the amount that was recorded in SG&A expenses as "lease payments" under the previous operating lease is now treated separately as depreciation and interest expense. Therefore, While operating income and EBITDA appear higher than before, net income is more likely to fluctuate due to the impact of interest expenses. become point should be noted.

Impact on cash flow statement (C/F)

Under the new lease accounting standard, the principal portion is classified as CF from financing activities and the interest portion is classified as either CF from operating activities or CF from financing activities, while all lease payments were previously included in CF from operating activities. As a result, operating activities CF tends to increase and financing activities CF tends to decrease. The financial indicators also change significantly.

Impact on financial indicators

There are also significant changes in financial indicators. First, the Equity ratio ratio tends to decline as total assets swell and the denominator increases due to the recording of new lease liabilities. In addition, ROA (return on assets) ROA (return on assets) may also decrease due to the increase in total assets. On the other hand, ROA (return on assets) may also decrease due to the increase in total assets, EBITDA is likely to increase because lease payments are excluded from SG&A expenses and broken down into depreciation and interest expense. This is especially true for industries with large lease contracts, such as real estate, airlines, and shipping.

Impact on disclosures (notes)

Under the new lease accounting standard, the information required to be disclosed will be significantly expanded. In particular, the new lease accounting standard requires disclosure of information that is directly related to financial forecasts, such as Lease-related balances and future cash flows and other information that is directly related to financial forecasts. The main items are as follows

- Information on accounting policies

- Information on lease-specific transactions

- Cash flows related to future lease payments

- Information to understand the amount of leases in the current period and subsequent periods

These disclosures will allow investors and financial institutions to better understand a company's contractual terms and future cash flow projections. On the other hand, companies will need to strengthen their systems for collecting and managing note information, and the practical burden on accounting departments will certainly increase.

Key Points of this Chapter

- In the balance sheet, assets and liabilities will increase, and the equity ratio will decrease.

- In the income statement, operating income and EBITDA will rise, and net income is likely to fluctuate.

- On the cash flow statement, CF from operating activities will increase and CF from financing activities will decrease.

- Financial indicators tend to decrease in ROA and increase in EBITDA.

- Disclosures will be expanded to include more detailed information on balances and future cash flows.

6. practical issues and impact by industry

The introduction of the new lease accounting standard will require not only changes in journal entries and accounting procedures, but also contract management, system operation, and even cross-organizational responses. Here we summarize the main practical issues and the degree of impact by industry sector.

Comprehensive understanding of contracts

Even if a "lease contract" or "rental contract" is not specified as a lease, if it is judged to be a lease in substance, it will be subject to on-balance sheet treatment. Therefore, it is necessary to collect and scrutinize contracts held not only by the accounting department but also by each department across the board.

Estimation of lease terms and discount rates

The exercisability of extensions and termination options must be rationally evaluated. Especially for those contracts that are subject to renewal, such as real estate contracts, it is expected that the accounting treatment will be based on a different term from the term stated in the contract. As for the discount rate, careful consideration is required as to how to use the company's own additional borrowing interest rate, etc. in the lease liability calculation.

Contract modification and re-estimation

Each time there is a rent revision, a change in contract terms, or a mid-term termination, the lease liability and the right-of-use asset should be recalculated and the journal entries and notes should be revised. In addition, the possibility of exercising extension or termination options should be reasonably evaluated, especially for real estate contracts that are subject to renewal, and it is expected that they will be accounted for over a different term from that in the contract. As for the discount rate, careful consideration is required as to how to use the company's own additional borrowing interest rate, etc. in the calculation of lease liabilities.

Consistency across the consolidated group

It is important that the entire group, not just a stand-alone entity, be unified in its response to the new lease accounting standard. If domestic and foreign subsidiaries, including domestic and foreign subsidiaries, have different judgments in determining leases, estimating lease terms, and setting discount rates, inconsistencies will occur in the consolidated financial statements. Therefore, a common policy should be established and the format for collecting contract information and reporting procedures should be standardized.

Compliance with other accounting standards and audits

Right-of-use assets recognized in lease accounting are subject to impairment accounting, and lease liabilities also affect tax accounting and the calculation of cost of capital. Therefore, it is necessary to consider the possibility that changes in lease accounting may spill over to other accounting standards. In addition, a company should have a system in place to explain to auditors the basis for its policies and estimates, as well as the calculation logic of the system.

Impact by industry (example of characteristics)

- Real estate business

If there are many leased master lease agreements, the impact will be very large because almost all properties operated in the business will be on-balance sheet. (No impact for those without master lease agreements, real estate management companies, etc.) - Multi-store retail and service companies

Since the company owns a large number of real estate properties as stores, the impact will be based on the number of stores. In addition, since it is necessary to assess each store for impairment, the burden on peripheral operations is also likely to be significant. - Shipping and airline industry

Aircraft and charter leases, which have been excluded from the on-balance sheet, are likely to be subject to this rule, and the impact on business is expected to be very large.

Compliance with the new lease accounting standards involves not only a simple review of accounting procedures, but also a wide range of issues, such as contract management systems, system compatibility, and group-wide policy unification. The impact will be particularly noticeable for industries with a large number of contracts or large contract amounts, and it is essential that a system be put in place as soon as possible.

Key Points of this Chapter

- There will be a wide range of issues such as contract management, discount rate estimation, and handling contract changes.

- Group-wide policies need to be unified, and consideration should be given to other accounting standards and audit compliance.

- Real estate and retailers have a large number of contracts, while shipping and airline companies have a large scale of contracts and a large impact.

- The financial and manufacturing industries also need to organize contract information and centrally manage ledgers.

- The earlier the number of contracts and the amount of money involved, the more essential it is to establish a system.

7. preparation for the new lease accounting standard and system support (steps to be taken for the application in 2027)

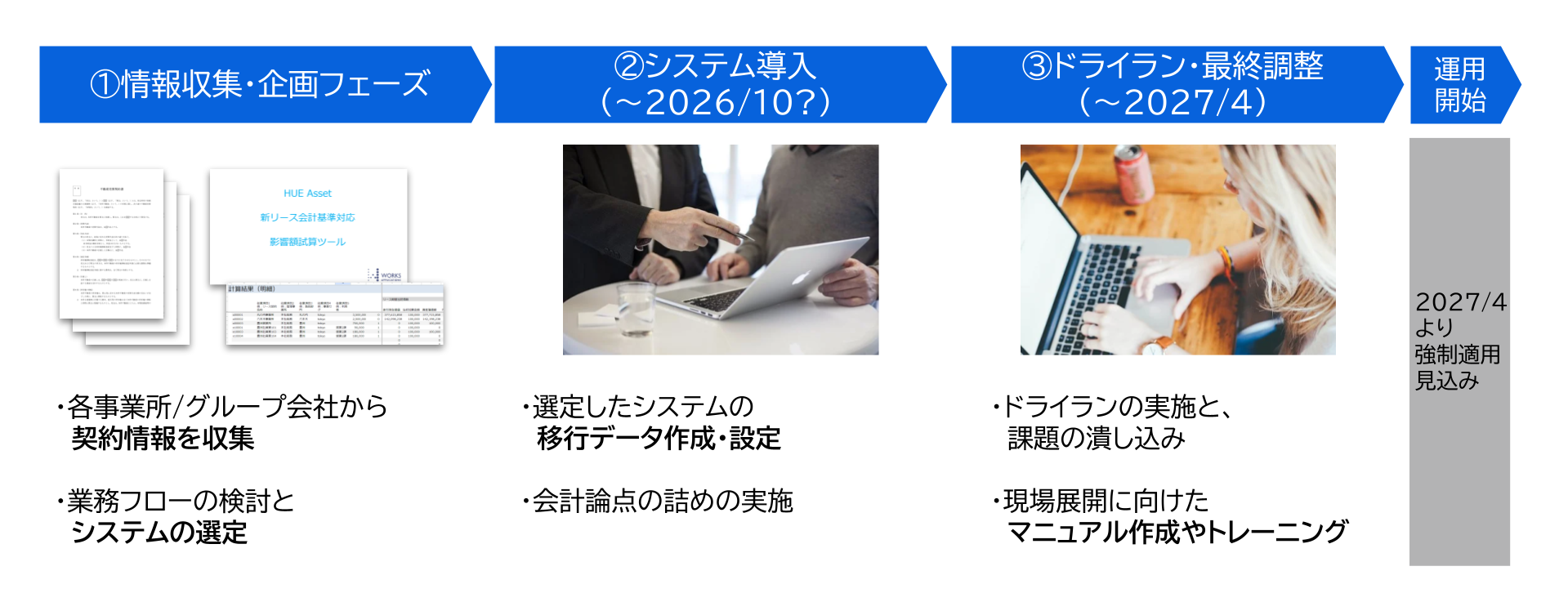

The new lease accounting standards will be mandatorily applied from April 2027, so it is essential that sufficient preparations be made by then. Since there is a limited period of time before the start of application, it is important to proceed in a systematic step-by-step manner.

Phase 1: Information gathering and planning

Even if they are not specified as leases or rental contracts, there are contracts that should be recognized as leases in substance among the transactions in which they are effectively leased or rented, and a company-wide inventory of contracts is required to identify these contracts. In addition, we will estimate the financial impact of major contracts and ascertain the impact on assets, liabilities, and key indicators. The results should be shared with management and relevant departments to provide a basis for policy decisions and explanations to stakeholders.

At this stage, it is also desirable to review the workflow and plan for the future introduction of the system. In order to facilitate practical responses, it is effective to utilize tools that enable efficient collection of contract information and trial calculation of the impact.

Phase 2: System implementation

Since the new lease accounting standards require a large number of contracts, changes in terms and conditions, and frequent re-estimates, manual management is not practical. Therefore, it is necessary to plan for system implementation from an early stage and proceed with the preparation and setup of transition data.

- Centralized management of contract ledgers

A system is required to register and manage contract information in one place and automatically generate present value calculations and journal entries by entering lease terms, discount rates, and payment terms. - Automation of contract modification and re-quotation

The system must be able to automatically reflect recalculations when renewals, mid-term terminations, rent revisions, etc. occur. - Support for subleasing

The system must be able to manage the entire contract lifecycle, including both lessee and lessor processing. - Management of Tax Association Discrepancies

The system must be able to maintain both accounting and tax amounts at the same time and automatically create a deductible expense schedule. - Utilization of AI, etc.

A system that can import contracts and automatically determine the conditions for lease eligibility would greatly reduce the man-hours required for contract inventory and data entry. - Internal Control and Audit Trail

It is necessary to make it possible to trace the calculation logic and the basis for discount rates, and to clarify the approval flow. A system must be in place that can be explained to auditors.

Phase 3: Dry run and final adjustment

Once the policy is decided and the system is in place, a dry run (simulated closing) is conducted using actual contract data. This will allow you to confirm the numerical impact and notes in advance and identify issues early on. It is also effective as an opportunity to obtain prior agreement with the auditor.

In addition, operation manuals and checklists should be prepared, and education and training should be provided not only to accounting staff but also to the entire group. It is also important to update the consolidation package and standardize reporting formats and workflow.

Phase 4: Operational launch

On the first day of adoption, the beginning journal entries should be posted and accounting treatment based on the new standard should begin. Since contract changes and re-estimates often occur during the period, systems and procedures must be in place in advance to respond immediately. In addition, it is necessary to establish operations that can withstand actual financial closing, including the preparation of notes and disclosures.

Quick Checklist

- Is there an inventory of contracts and a policy for determining leases?

- Has the company established internal standards for the period, discount rate, short term/small amount, and simplified treatment of leases?

- Have templates for present value calculations, journal entries, and notes been designed?

- Do you have procedures in place for dealing with contract changes and re-estimates?

- Has a dry run been conducted and agreed upon in advance by the auditor?

- Are the system requirements (centralized ledger, recalculation, tax discrepancy management, and evidence trail) met?

The time left until the new lease accounting standard is applied is limited. Preparations must be made systematically based on the following steps: inventory of contracts, estimation of impact, system implementation, dry run, and production application. In particular, system development and establishment of internal controls are essential for efficient and accurate accounting processes that are becoming increasingly complex.

Key Points of this Chapter

- In preparation for the start of application, an inventory of contracts and an understanding of their impact is necessary.

- System implementation and internal controls are essential to streamline accounting and contract management.

- Before full-scale application, it is important to confirm issues through mock accounts and promote agreement with and education of auditors.

- A system that can be operated from the first day of application should be established, and preparations should be made to accommodate contract changes and note preparation.

Summary: Pillars of response and recent actions

The new lease accounting standard is a major systemic revision that in principle requires lessees to account for lease transactions on-balance. Contracts that were previously expensed off-balance sheet will now be required to recognize a right-of-use asset and a lease liability on the balance sheet. As a result, the way financial statements look, key management indicators, and even the scope of notes will change significantly.

The four pillars of the response can be summarized as follows.

- Inventory of contracts and understanding of their impact

It is necessary to identify company-wide contracts that fall under leases, regardless of name, and estimate the impact on financial statements and management indicators. - Develop policies and implement systems

It is required to unify internal policies on lease determination, term estimation, discount rate, and treatment of short term and small amount leases, etc., and to implement and prepare a system in accordance with such policies. - Dry Run and Final Adjustment

Mock financial statements using actual contract data should be performed to verify the numerical impact and note contents in advance. It is also important to build consensus with auditors and prepare group-wide education and training at this stage. - Production application and establishment of an operational system

On the first day of application, the journal entries at the beginning of the period must be recorded, and a system must be in place to respond immediately to contract changes and re-estimates during the period. In addition, it is necessary to establish internal controls and build an environment that can withstand audits and explanations to investors.

Finally, the most recent actions are summarized below.

-

Understanding the subject contract (the first starting point)

First, early identification of contracts subject to on-balance sheet treatment provides a clear starting point for preparation. -

Estimate the impact (essential for reporting to management and responding to investors)

By understanding the impact on assets, liabilities, and key indicators, and sharing this information with management, we can prepare the necessary materials for decision-making. -

Develop internal policies and system plans (directly related to internal controls)

It is essential to unify the treatment of decision criteria and discount rates so that the system can support practical operations. -

Prepare a dry-run plan (necessary to prepare for audits and actual operations)

Issues will be identified in advance through simulated closing, leading to agreement with and education of auditors.

These are the actions that should be prioritized within the limited preparation period and are the first steps to support the transition to the new lease accounting standards. It is required to check your company's situation now and make preparations in a systematic manner.

We hope that this article will be of help to you in making a smooth transition to the new lease accounting standards.

Supervisor: Mr. Masahiko Inoue (Certified Public Accountant)

As a partner of an audit firm, Mr. Inoue has been involved in auditing and advisory services related to leasing for many years. He is a former leader of the audit firm Tomatsu Lease Credit Industry Leasing Leader and currently serves as a senior fellow in charge of leases at the Accounting Education and Training Organization of Japan in cooperation with the Japanese Institute of Certified Public Accountants (JICPA). He has published a total of eight books on lease accounting taxation in his main publications (most recently, "New Lease Accounting Practical Response and Intuition" published at the end of February 2025). He has served as a training instructor for the Leasing Business Association for many years and has experience as a leasing training instructor in over 30 cases.

Reference: List of free tools and materials to support compliance with the new lease accounting standards

- Contract collection sheet (streamlines the organization and management of contract information)

- Impact amount estimation tool (simulate impact on financial indicators)

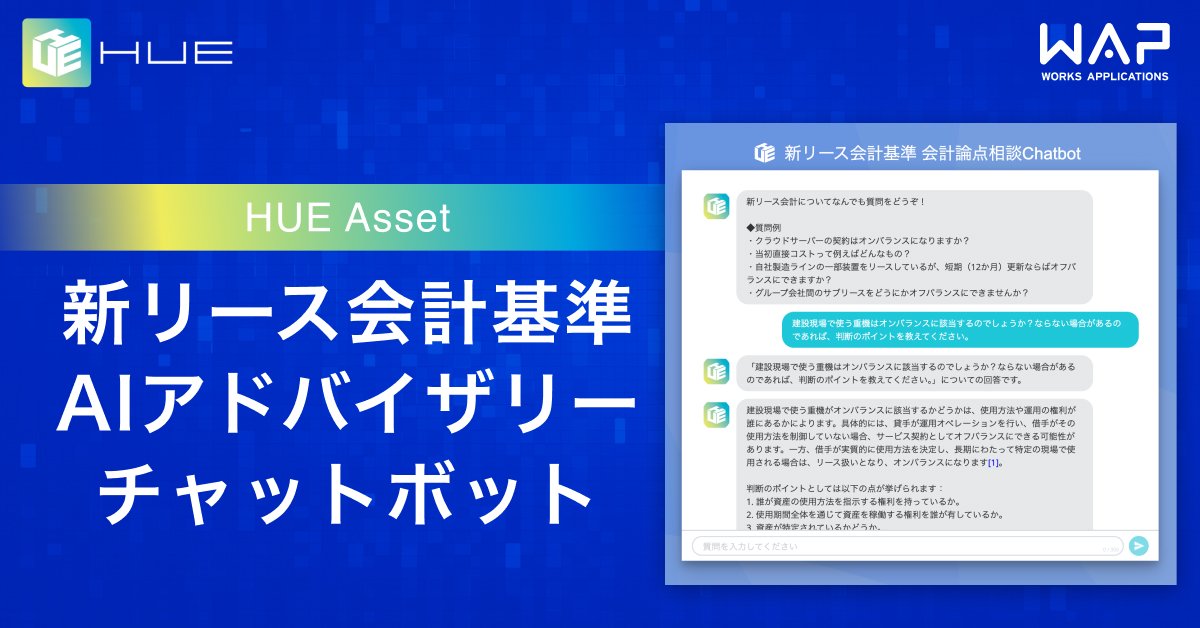

- AI advisory chatbot (immediate response to consultation on accounting issues)

White Paper

Masahiko Inoue, Certified Public Accountant supervised by

New Lease Accounting Standards Contract Collection Sheet

Download ArielAirOne

White Paper

New Lease Accounting Standards: Impact Calculation Tool

Download ArielAirOne

White Paper

Masahiko Inoue, Certified Public Accountant / supervised by Masahiko Inoue / New Lease Accounting Standards AI Advisory Chatbot

Download ArielAirOne

Related articles:

Three conditions for using the ¥3 million standard in the new lease accounting

How to set the lease term under IFRS 16? [Survey of major companies]

What journal entries and accounting procedures are required under IFRS 16 (New Lease Accounting Standard)?

The new lease accounting standard is explained in an easy-to-understand manner! How does it differ from the current standard?

When will the new lease accounting standard become effective? Explanation of the expected timing from the exposure draft!

Related Useful Information

White Paper

2026/02/06

The new lease accounting "business flow" design guide with sample flows.

Web Articles

Jan 30, 2026

How far can you go against the auditors? Real-life battle of new lease accounting and "behind-the-scenes" criteria for system selection revealed by a professional.

Web Articles

2026/01/21

Explanation of the 2026 Tax Reform Proposal for Accounting and Finance - What will change from a practical perspective? What are the changes from a practical perspective?

Related Case Studies

Halved the number of man-hours required to manage fixed and leased assets

JACCS Corporation

![]()

Business Reforms with HUE, which Supports Accounting for School Corporations with Standard Functions

Ritsumeikan University Educational Corporation

Adoption of HUE to reduce IT investment costs and achieve sustainable growth

NITTETSU CHEMICAL & MATERIAL Co.