Web Articles New lease accounting standard

2020/10/06

When will the new lease accounting standards become effective? Explanation of the expected timing from the exposure draft!

In May 2023, the ASBJ (Accounting Standards Board of Japan) issued an exposure draft of the new lease accounting standard. This standard follows in principle IFRS 16, which has already been initiated by companies that have voluntarily adopted IFRS, and will be applied by all Japanese companies, which may have a significant impact on their accounting treatment.

This article will provide an overview of the new lease accounting standard, the relationship between IFRS and Japanese GAAP, and when it will be mandatorily applied. (Last updated on November 15, 2023)

Table of Contents

What is the new lease accounting standard?

First, we will provide an overview of what will change under the new lease accounting standard based on the exposure draft released by the ASBJ (Accounting Standards Board of Japan) in May 2023.

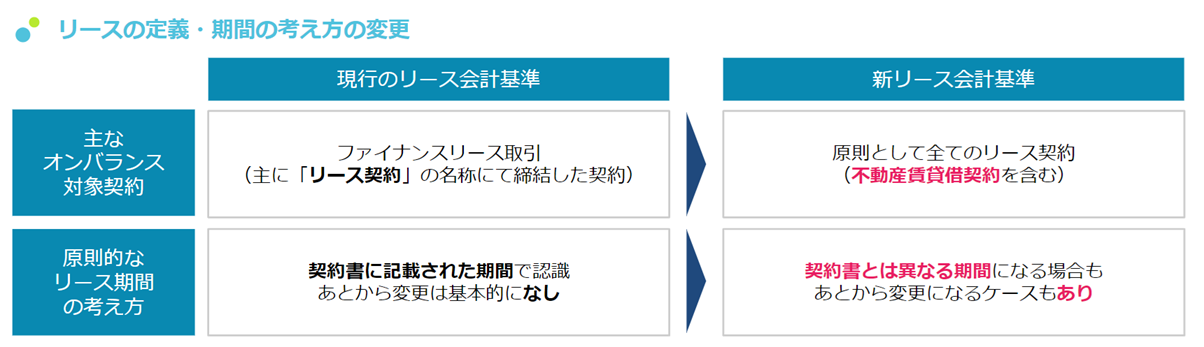

Change 1: Increase in the number of assets to be accounted for on-balance sheet

Under the previous Japanese accounting standards, in order for a lease to be treated as a "finance lease" subject to on-balance sheet treatment, it had to satisfy the conditions of "non-cancelable before maturity" and "full payout".

Under the new lease accounting standard, however, this criterion has been eliminated. If a lease meets the conditions of "not small amount (over 3 million yen)" and "not short term (over 1 year)", it will be subject to on-balance sheet treatment. Therefore, leased properties such as offices and stores are also subject to on-balance sheet treatment, which will significantly increase the number of leases under management for some companies.

Change 2: Change in the concept of the lease term

In addition, the method of calculating lease term has also been changed. While in the past, a lessee was only required to account for leases based on the contract term, the new lease accounting standard requires that the lease term be measured based on "extension options (whether or not to extend the contract)" and "termination options (whether or not to terminate the contract in the middle of the lease term)". Therefore, there are many matters to be considered in accounting for leases, and consideration of corresponding policies is required.

Related document: How to interpret the standard in practice? IFRS 16 Application Status Report

Related article: IFRS 16 (New Lease Accounting Standard) Explained in an Easy-to-Understand Way! How does it differ from Japanese GAAP?

Why are the lease accounting standards changing?

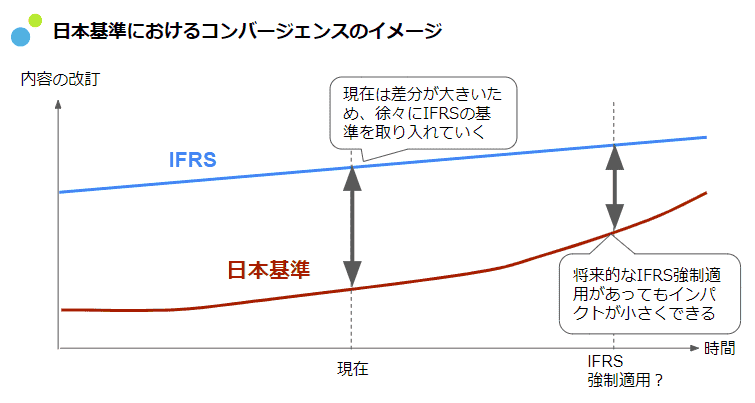

But why is the previous lease accounting standard being updated and why is the transition to the new lease accounting standard underway? The reason lies in the "convergence" that Japanese accounting standards are promoting.

What is convergence?

Since the 2000s, Japan and other countries that had their own accounting standards, such as the United States, have been required to take actions to ensure comparability with foreign companies. In response, countries have adopted the policy of "applying IFRS to all companies in the country" or "changing the accounting standards in the country to those similar to IFRS (= convergence). Convergence is a response to this background to enable accounting comparisons between home and foreign companies.

Japan and the status of implementation of convergence

Japan currently has a policy of convergence, and major changes made in IFRS are often applied to Japanese GAAP.

Most recently, the Revenue Recognition Standard, which changes the timing of revenue recognition, has been applied to Japanese GAAP in a largely unchanged form.

As for leases, "IFRS 16" changes the guideline for on-balance-sheet leases from the fiscal period ending March 2020 onward, and the difference between IFRS 16 and Japanese GAAP is currently widening.

In order to apply the changes to Japanese GAAP and reduce the difference, the changes are expected to be applied to Japanese GAAP again, this time in a format almost the same as IFRS 16.

When will it be applied to Japanese GAAP?

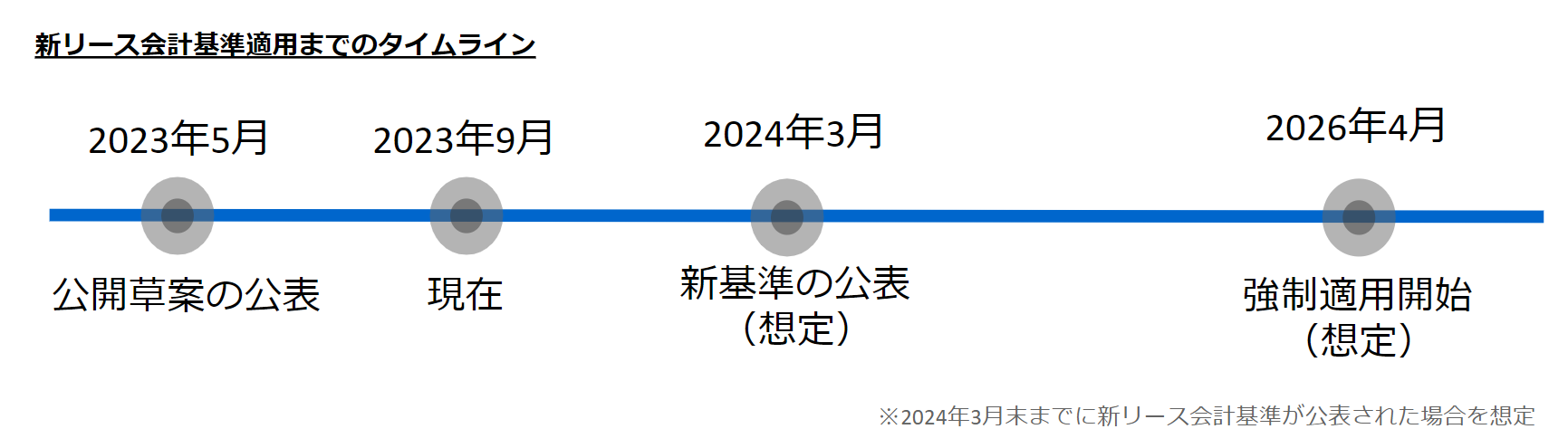

So when will the "new lease accounting standard" be applied to Japanese GAAP? The answer is still undecided, but it is highly likely that the new lease accounting standard will be applied in April 2026 at the earliest.

Announced by ASBJ (Accounting Standards Board of Japan)

As of November 2023, the ASBJ has not yet announced the specific date of application of the new lease accounting standard.

On the other hand, however, the ASBJ has stated that in principle the new lease accounting standard will be applied from "the beginning of consolidated fiscal years and fiscal years beginning on or after approximately two years after the date of the issuance of the accounting standard.

The timing of the "release of the accounting standard" has not yet been named, but it is said that it is highly likely to be released by the end of March 2024.

What will be the actual application timing?

Given the above situation, if the new lease accounting standard is released by the end of March 2024, all Japanese companies may be required to comply with it as early as the fiscal year beginning April 2026.

It is also proposed to allow early adoption.

Since the new lease accounting standard will affect a large number of assets, and there will be many items to be considered in accounting treatment, it is necessary to consider now how to respond to the new lease accounting standard, such as "whether to respond with Excel" or "whether to consider responding with a system".

Utilize a system that is compatible with the new lease accounting standards.

Finally, for those who are considering a policy to comply with the new lease accounting standards, we would like to introduce our recommended products.

For large companies Fixed asset management system HUE Asset HUE Asset will support operations under the new lease accounting standards with standard functions, such as re-estimation of recorded amounts and linkage of lease contract data to lease contract data.

HUE Asset's solution for the new lease accounting standard is as follows, IFRS 16 Application Report The solution for HUE Asset's new lease accounting standard is also introduced in the IFRS 16 Application Fact Sheet. If you are interested, please download and review the report.

Related articles:

To request HUE Asset information, please visit

Related Useful Information

Web Articles

Jan 30, 2026

How far can you go against the auditors? Real-life battle of new lease accounting and "behind-the-scenes" criteria for system selection revealed by a professional.

Web Articles

2026/01/21

Explanation of the 2026 Tax Reform Proposal for Accounting and Finance - What will change from a practical perspective? What are the changes from a practical perspective?

Web Articles

2025/11/28

Companies Subject to the New Lease Accounting Standards [Quick Reference] and What Subject Companies Need to Keep in Mind

Related Case Studies

Nankai Electric Railway x WAP talks about the "overwhelming return generated by 'add-on zero ERP'".

Nankai Electric Railway Co.

![]()

Nankai Electric Railway introduces HUE DI and upgrades HUE, Building a Management Foundation that Continues to Adapt to Change

Nankai Electric Railway Co.

![]()

Inventory preparation man-hours drastically reduced. HUE" in a few hours

Huis Ten Bosch Corporation

![]()