Web Articles New lease accounting standard

2024/07/15

Three Conditions for Using the ¥3 Million Standard in New Lease Accounting

In May 2023, the ASBJ (Accounting Standards Board of Japan) issued an exposure draft of a new lease accounting standard. Under the new standard, in principle, all lease contracts must be treated as on-balance sheet, while the so-called "3 million yen standard" is expected to be maintained, so many companies may find that their on-balance sheet targets differ significantly depending on how the small amount determination can be applied.

This article provides an overview of the new lease accounting standard and explains in detail the conditions that should be considered when applying the ¥3 million standard.

Table of Contents

Overview of the "3 Million Yen Standard" in the New Lease Accounting Standard

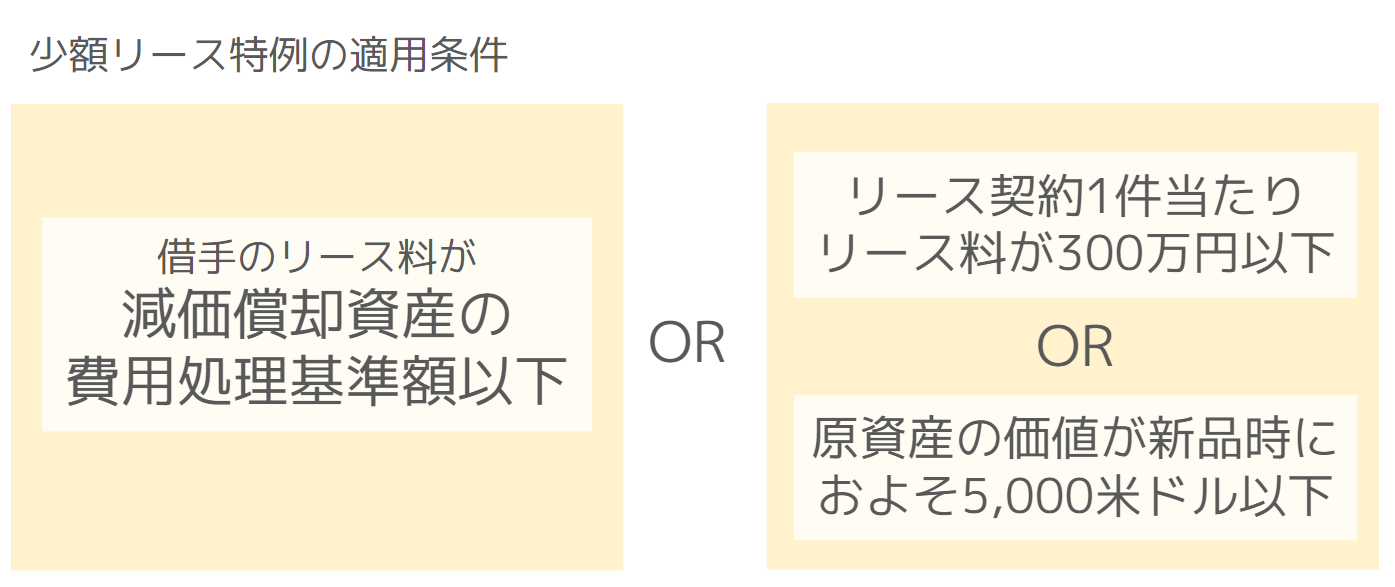

Under the exposure draft of the new lease accounting standard released by ASBJ (Accounting Standards Board of Japan) in May 2023, all lease contracts are to be accounted for as on-balance sheet in principle, while off-balance sheet treatment is permitted for small value lease contracts under the following conditions (1) A lessee is allowed to treat all lease contracts as on-balance sheet as a general rule.

The amount of the total lease payments is less than or equal to the amount of the standard amount of depreciation expense" is generally read as "less than or equal to 200,000 yen (less than or equal to the amount of the standard amount of fixed assets)". Since the "3,000,000 yen standard" described below tends to have a higher upper limit, the actual use of this standard is considered to be limited.

The "lease payments of 3 million yen or less per lease contract" is a continuation of the current 3 million yen standard. It is inherited together with other special exceptions such as re-leases and short-term leases, and can be removed from the on-balance sheet depending on the total lease payments.

Also, it should be noted that "the value of the underlying asset is approximately US$5,000 or less when new" is inherited from the accounting treatment in IFRS 16, and only this criterion requires the determination of the value of the underlying asset based on the "market value of new equipment" rather than the total lease payments.

Considering these conditions, it is highly likely that many companies will mainly judge the lease contracts based on "the lease payments per lease contract are less than 3 million yen" (= 3 million yen standard ).

Related page

Three conditions to be considered for using the ¥3 million standard

The number of contracts subject to on-balance sheet accounting is probably one of the most important points for each company when applying the new lease accounting standard, and the details of the application criteria are important because the number of contracts subject to on-balance sheet accounting may change significantly when the ¥3 million standard is used. Below are three conditions that should be considered when applying the ¥3 million standard.

1. judgment on the total amount within the contract years

It is important to judge the total lease payments over the entire contract period, not only by a single month's lease payments. As shown in the table below, even if the monthly lease payments are the same, the applicability of the 3 million yen criterion will vary depending on the contract period.

|

Contract Term |

Monthly Lease Payments |

Total lease payments |

Determination |

|

2 years |

120,000 yen |

2,880,000 yen |

Off-balance sheet |

|

5 years |

120,000 yen |

7.2 million yen |

On-balance sheet |

For example, if the monthly lease payment is 120,000 yen for a two-year lease contract, the total amount of the lease payment would be 2,880,000 yen, which meets the 3,000,000 yen criterion. However, if the same monthly lease fee is contracted for 5 years, the total amount would be 7.2 million yen and would not meet the 3 million yen criterion.

2. judgment of the total amount in the contract unit

The determination must be made on a contract-by-contract basis, not on a property-by-property basis. As shown in the table below, even if a single property alone does not meet the 3 million yen standard, the standard may be exceeded when the entire contract including multiple properties is considered.

|

Property included in the contract |

Property Lease Payments |

Total Monthly Lease Payments |

Total annual amount |

Total lease payments (5 years) |

Determination |

|

Property A |

50,000 yen per month |

50,000 yen |

600,000 yen |

3 million yen |

If you look at this property alone, it is off-balance sheet |

|

Property B |

40,000 yen per month |

40,000 yen |

480,000 yen |

2.4 million yen |

If you look at this property alone, it is off-balance sheet |

|

Entire contract |

90,000 yen |

1,080,000 yen |

5.4 million yen |

On-balance sheet |

For example, if the monthly lease fee for Property A is 50,000 yen and the monthly lease fee for Property B is 40,000 yen, each property alone meets the 3 million yen standard.

However, if Property A and Property B included in the same contract are combined, the total amount over 5 years would be 5.4 million yen, and the contract as a whole would not meet the 3 million yen criterion.

3. including tax or excluding tax? Excluding tax? Determine consumption tax properly

Many people are concerned about whether the tax is included or excluded, but surprisingly, there is no explicit provision on this point.

The reason for this is said to be that "this is only one criterion to judge the materiality of a contract, and an important contract should be on-balance sheet even if it is less than 3 million yen".

It is important to proceed after establishing the rules for operating within the company.

Which contracts are subject to the ¥3 million standard?

So, what are the contracts that can and cannot be excluded from the on-balance sheet as a result of actually applying the 3 million yen standard?

First of all, many of the contracts for general office automation equipment, car leases, machinery leases, etc. are already accounted for in accordance with the 3 million yen standard.

On the other hand, real estate lease contracts were not subject to the on-balance sheet judgment until the new standard was applied, so it is necessary to carefully consider whether the 3 million yen standard is applicable or not. In many cases, the total amount of large lease contracts such as for head office buildings is likely to exceed 3 million yen, but there are cases in which some offices and sales offices may be subject to the application of the new standard, so consideration is necessary.

When the number of on-balance sheet contracts is large, there is a limit to managing them with Excel, so consideration should be given to introducing a system.

HUE Asset , a fixed asset management system for large companies, supports operations under the new lease accounting standards with standard functions such as re-estimation of recorded amounts and linkage of lease contract data to lease contract data.

We provide information on legal revision trends, including reports summarizing trends at each company at the time of IFRS 16. We are continuously providing information on the trend of legal changes, such as a report summarizing the trend of each company at the time of IFRS 16. If you are interested, please download and review the report.

Related article:

Related Useful Information

Web Articles

Jan 30, 2026

How far can you go against the auditors? Real-life battle of new lease accounting and "behind-the-scenes" criteria for system selection revealed by a professional.

Web Articles

2026/01/21

Explanation of the 2026 Tax Reform Proposal for Accounting and Finance - What will change from a practical perspective? What are the changes from a practical perspective?

Web Articles

2025/11/28

Companies Subject to the New Lease Accounting Standards [Quick Reference] and What Subject Companies Need to Keep in Mind

Related Case Studies

Nankai Electric Railway x WAP talks about the "overwhelming return generated by 'add-on zero ERP'".

Nankai Electric Railway Co.

![]()

Nankai Electric Railway introduces HUE DI and upgrades HUE, Building a Management Foundation that Continues to Adapt to Change

Nankai Electric Railway Co.

![]()

Inventory preparation man-hours drastically reduced. HUE" in a few hours

Huis Ten Bosch Corporation

![]()