Web Articles New lease accounting standard

2021/04/05

How to Set the Lease Term under IFRS 16? A Survey of Major Companies in Japan

The new lease accounting standard (=IFRS 16) has started mandatory application for companies that have voluntarily applied IFRS.

However, since IFRS only describes standards in principle, actual accounting policies differ from company to company. In particular, there are many cases where various decisions are made on how to set lease terms, especially on "how much to take into account other than the contract term".

In this article, based on the results of the "IFRS 16 Application Fact-Finding Survey" conducted independently by Works Applications, we will provide information on how to set lease terms based on actual examples.

Table of Contents

Concept of lease term in IFRS 16 (new lease accounting standard)

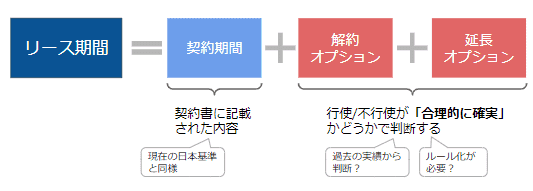

The new lease accounting standard requires that the lease term be determined not only by the "term stated in the contract" but also by considering "cancellation options" and"extension options" (i.e., the lease term should be shorter if the lessee is likely to cancel the lease in the middle of the term, and longer if the lessee is likely to extend the term). The company is asking for this.

The reason behind this change is the change in contracts subject to on-balance sheet recognition. Under the previous standard, "finance leases " have been accounted for on-balance sheet. Since finance leases were assumed to be "substantially the same as the purchase of an asset with debt," there were few cases where the terms of the contract changed during the term of the lease.

However, under the new lease accounting standard, "real estate" is also subject to the new lease accounting standard, so the content and term of the contract will become more fluid, such as "a contract was to be for two years but was extended" or "the rent will be reduced in the middle of the contract because it is a long-term contract.

Therefore, IFRS 16 requires the lease term to take into account options such as cancellation and extension.

Related page

Actual situation of how lease terms are set by major companies

As described above, IFRS 16 changes the concept of lease term. However, there is no specific guideline for determining the actual lease term, and it is often the case that each company operates separately while consulting with their auditors.

Therefore, here, based on the "IFRS 16 Application Survey Report" conducted independently by Works Applications, we would like to provide an actual example of how each company sets the lease term.

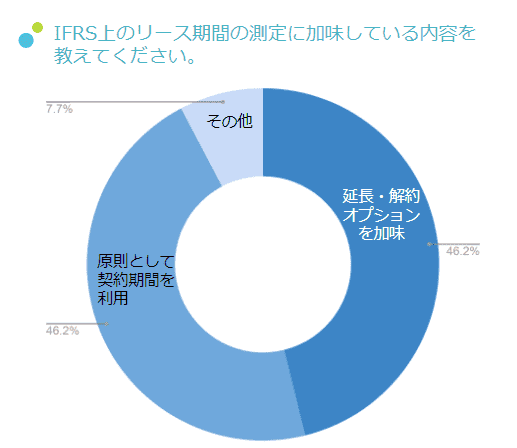

Fact (1) Concept of lease term

One of the issues in the lease term is how to consider "extension and cancellation options". According to the survey results, while many companies consider extension and cancellation options, half of the companies use the lease term as the contract term in effect.

Companies with a smaller number of contracts tended to be more willing to consider extension/termination options, while companies with a larger number of contracts tended to balance the options by taking into account actual operations.

Comments

・The number of cases was also small, so we considered filling in each asset, but in the end we could not come up with a proper rule (manufacturing industry)

・" Actual situation" is a numbers game no matter how much we discuss it, so we unified with the contract period. " Since "extension" requires the consent of both parties, it cannot be said that "renewal is definitely expected" (transportation industry)

・ Only for offices, 13 years (average) was used. The rest of the contract period was set as the contract period (service industry)

・In the APM, it was stated that "If it is not in accordance with the actual situation, it will be revised upon approval", but in practice, it was designed to be only the number of contract years (manufacturing industry).

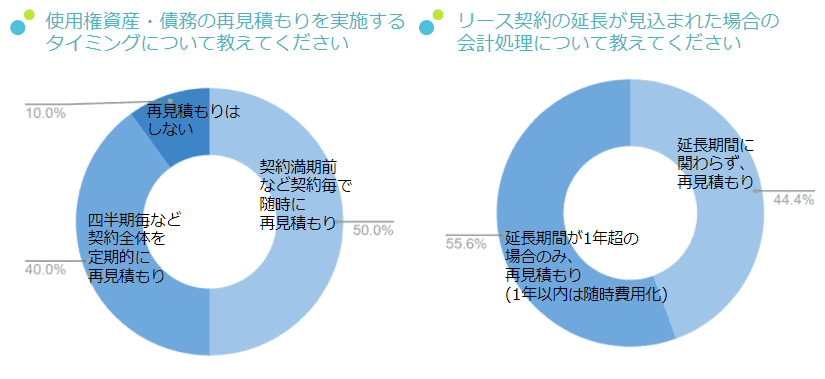

(2) Treatment of re-estimation

Another point of contention regarding lease term is the treatment of "re-estimation," which is said to be performed when a contract is later extended. Half of the respondents answered that they "re-estimate at any time or at the timing of calculating the financial figures." Some said that they plan to re-estimate the lease term and liabilities when the contract is extended.

On the other hand, many respondents said that they have never implemented it because it is just after the application of the new lease accounting standards, or that the detailed operation has not been decided yet, and there were many responses based on the assumption that the operation has not been decided yet.

Comments

・Re-estimate in case of contract renewal (retail industry)

・Actions to be taken in case of renewal have not yet been determined since there are no contracts that are up for renewal yet. Re-estimate in case of rent revision. (Retail industry)

・Contracts scheduled for renewal are checked every quarter. (Manufacturing)

・Currently, the number of properties is small, so in principle, contracts are reconsidered on an annual basis. (Manufacturing)

・It is recognized that quarterly review is desirable, but it is likely to be a time-specific approach, such as when actual renewals are due (service industry).

The first step in response to IFRS 16 (New Lease Accounting Standard) is to know the "actual situation".

As described above, in dealing with the new lease accounting standard, knowing the "actual situation"such as "other companies are not dealing with it for some reason" or "other companies are still struggling to deal with it," reveals the true picture that cannot be seen only by the standard.

Although the treatment of the new lease accounting standard in Japanese accounting standards has not been finalized yet, it is highly likely that such "actual conditions" will be taken into account in the revision to which all Japanese companies will be subject, and that it will be finalized in a form that many companies can easily accept.

Although it is difficult to grasp the whole picture of the new lease accounting standard compared with the large amount of impact on the BS, the current situation is such that it is difficult to grasp the whole picture of the new lease accounting standard. However, it is possible to prepare for the new lease accounting standard by knowing the current situation, estimating the impact, and considering accounting policies.

The following is a summary of the results of the survey conducted by Works Applications, Inc. IFRS 16 Compliance Survey Report In addition to the "lease term" introduced in this blog, the report also provides a summary of the actual responses of major Japanese companies to more than 10 issues, including the "scope of assets accounted for as leases" and"status of systemization".

If you are a company applying IFRS and are concerned about examples of other companies, you can get a grasp of the "reality" that will underlie future revisions of the standard and learn how to respond. Please download and check it if you want to grasp the "actual situation" that will be the basis for future revision of the standard and to "prepare" for the revision.

Related articles:

- Even companies using Japanese GAAP must support this! When will the new lease accounting standard be applied?

- IFRS 16 (New Lease Accounting Standard) is explained in an easy-to-understand manner! How does it differ from Japanese GAAP?

To request HUE Asset information, please visit

Related Useful Information

Web Articles

Jan 30, 2026

How far can you go against the auditors? Real-life battle of new lease accounting and "behind-the-scenes" criteria for system selection revealed by a professional.

Web Articles

2026/01/21

Explanation of the 2026 Tax Reform Proposal for Accounting and Finance - What will change from a practical perspective? What are the changes from a practical perspective?

Web Articles

2025/11/28

Companies Subject to the New Lease Accounting Standards [Quick Reference] and What Subject Companies Need to Keep in Mind

Related Case Studies

Nankai Electric Railway x WAP talks about the "overwhelming return generated by 'add-on zero ERP'".

Nankai Electric Railway Co.

![]()

Nankai Electric Railway introduces HUE DI and upgrades HUE, Building a Management Foundation that Continues to Adapt to Change

Nankai Electric Railway Co.

![]()

Inventory preparation man-hours drastically reduced. HUE" in a few hours

Huis Ten Bosch Corporation

![]()