Web Articles New lease accounting standard

2025/11/28

New Lease Accounting Standard and Lease Contracts

This article explains how the new lease accounting standard will change lease contracts, especially real estate lease contracts, from a practical perspective. We hope that this article will help you to understand the impact of the new lease accounting standards and the increased burden on your practice, and to make a decision on how to respond to the new lease accounting standards in the future.

Table of Contents

How will the new lease accounting standard change real estate leases?

The new accounting standard will apply to real estate lease contracts for which rent should have been expensed on a case-by-case basis in the past. The new lease accounting standard will also apply to real estate lease contracts, for which rents were previously expensed as incurred, Many new journal entries will be required to be recorded. This will place a particularly heavy burden on companies that have a large number of operating lease transactions under the current standard. Furthermore, because subleases are classified based on the right-of-use asset recognized in the head lease rather than the underlying asset, not only the lessee, but also the lessor (intermediate lessor) of the sublease. This article is intended to provide an overview of the accounting treatment of real estate leases.

This article focuses on real estate leases. For a general overview of the background of the new lease accounting standard, timing of application, companies to which the standard will be applied, differences from the current system, and the impact on financial statements, please refer to the comprehensive explanation below.

![Complete Explanation] New Lease Accounting Standards Effective in 2027|Outline, Changes, Impact, and Practical Responses](/assets_c/2025/10/new-lease-2027_display.png)

1-1. Real estate lease contracts are also subject to the new accounting standard.

Under the new lease accounting standard, a lease is considered to be a lease if the lessee controls the use of the specified asset, even if the contract name is "rental" or "lease. Because the determination of the applicability of a lease is mainly based on the following three points, Real estate lease contracts are applicable and subject to on-balance sheet treatment in principle (1) The lease is a lease.

-

Specified assets (no substantial right of substitution)

An asset identified in the contract is indicated and the supplier has no substantial right of substitution. -

Enjoyment of the majority of economic benefits

The lessee enjoys the majority of the economic benefits derived from the asset throughout the term of the contract. - The right to direct the use

The right of the lessee to determine the purpose and method of use of the asset during the term of the contract.

In addition, common expenses, maintenance, cleaning, insurance, taxes and public dues, etc. Service charges are not subject to on-balance sheet treatment. Generally, they are separated from lease elements (e.g., rent) and treated as expenses. In separating them, reasonable allocation criteria such as area, time, number of units, fixed price list, etc. should be established in advance and consistently applied to similar contracts. For example, if common service charges are not specified in a "lump-sum billing of rent + common service charges," rules are established for presumptive allocation based on the exclusive area ratio or the management association's prorata table.

1-2. Many journal entries are required.

Under the new lease accounting standard, a real estate contract, etc., for which lease payments should have been made on a case-by-case basis in the past, Many journal entries are required, including journal entries to be recorded at the time the contract is concluded and journal entries to be made at the time the contract expires. At the inception date, the present value of future rentals is recognized as a lease liability, and the amount adjusted for initial direct costs, incentives, restoration, etc. is recognized as a right-of-use asset. In addition, at the time of payment, the journal entry must be prepared taking interest into account and monthly amortization calculations are also required, which is expected to increase the workload of the accounting department.

Please refer to the following article for specific journal entries and accounting procedures along with practical scenarios.

Lease terms must be estimated "in accordance with actual conditions

Under the new lease accounting standard, The lease term is estimated by adding or subtracting the expected exercise of extension/termination options to or from the term stated in the contract. For accounting purposes, even in the case of a real estate contract with an automatic one-year renewal, a lessee cannot expect renewal based on practice alone. Only to the extent that the extension can be supported by objective materials that are "reasonably certain" of an extension, the renewal period should be included in the lease term. The determination of the lease term should be documented by the commencement date, and the lease term should be revised if the assumptions change due to a formal decision to withdraw or a significant revision of the rent terms. The discount rate should be based on a reasonable estimate of the additional borrowing rate (IBR) consistent with the terms of the contract.

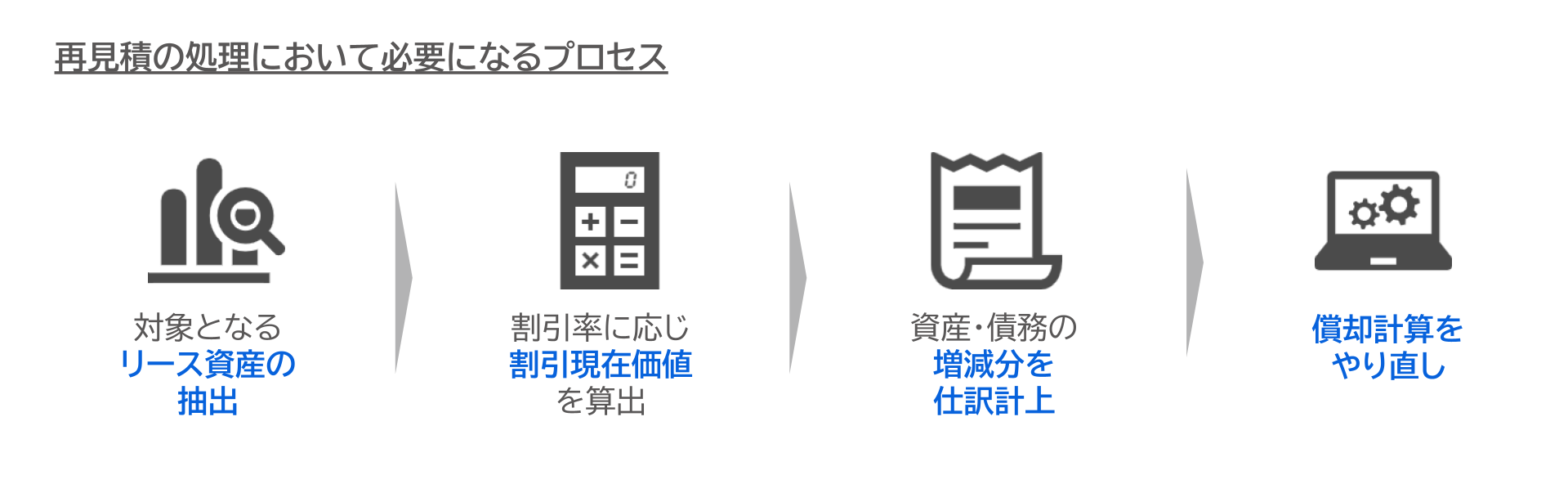

1-4. Increased burden of re-measuring/re-estimating

Under the new lease accounting standard, re-measurement is required according to changes or revisions during the period, and the difference is adjusted to the right-of-use asset in principle. If the reduction exceeds the balance of the right-of-use asset, the excess is recognized as a loss. In performing the re-measurement, In addition to the need to accurately obtain information on changes and extensions of contracts, detailed calculations that take interest into account are required. In addition, detailed calculations that take interest into account are required, which can be extremely burdensome.

2. what needs to be addressed specific to real estate

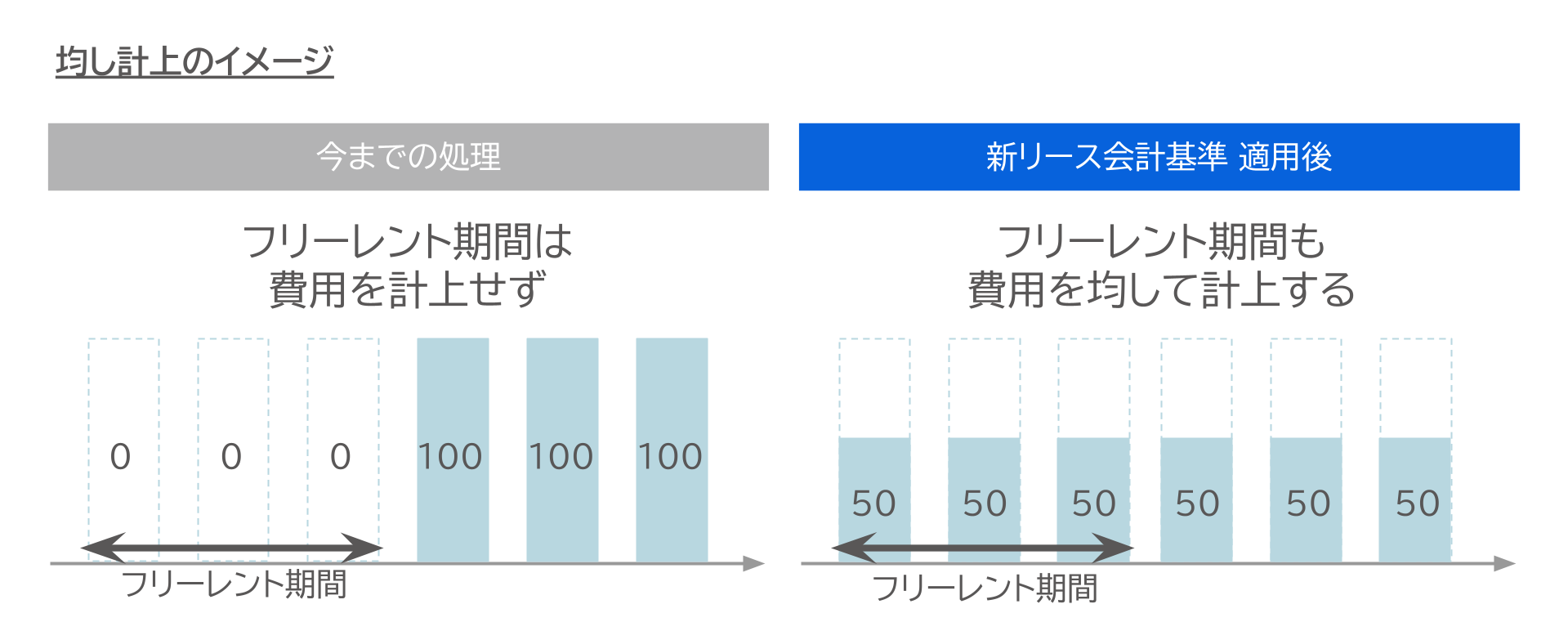

2-1. Free Rent and Phased Rent

In real estate leasing, free rent or step rent (step rent) immediately after occupancy is not uncommon. Even if the rent fluctuates during the term, the principle is to recognize income and expenses by leveling them over the entire term of the contract. The lessor recognizes revenue on a level basis, including the free rent period, and the lessee also factors incentives into the initial measurement and allocates expenses on a level basis over the term of the contract.

If the current accounting management system is based only on the simple posting of invoiced amounts, it will not be able to handle the automatic journal entries for the anticipation and advance payments required for free rent and step rent leveling, which will increase the operational burden and make it easier for input and posting errors to occur. It is a good idea to have a recording policy and system support in place in advance.

2-2. Security Deposit, Restoration, Short Term/Small Amount

For security deposits, the portion that is contractually clear that it will not be returned or the amount that is confirmed to be applied to rent is transferred to the cost of the right-of-use asset on the commencement date. The portion expected to be returned is transferred to the acquisition cost of the right-of-use asset at the time of payment.

If an obligation to restore the asset to its original condition is expected, the cost of removal, demolition, and restoration is estimated at the present value of the asset at the commencement date. The amount is recorded as an asset retirement obligation and the same amount is added to the right-of-use asset.

Internal criteria for short-term/minor amounts, along with the scope of application, should be documented in advance and consistent with audit and taxation. Short-term is usually 12 months or less, while small amounts are based on monetary criteria and the scope of assets to be excluded.

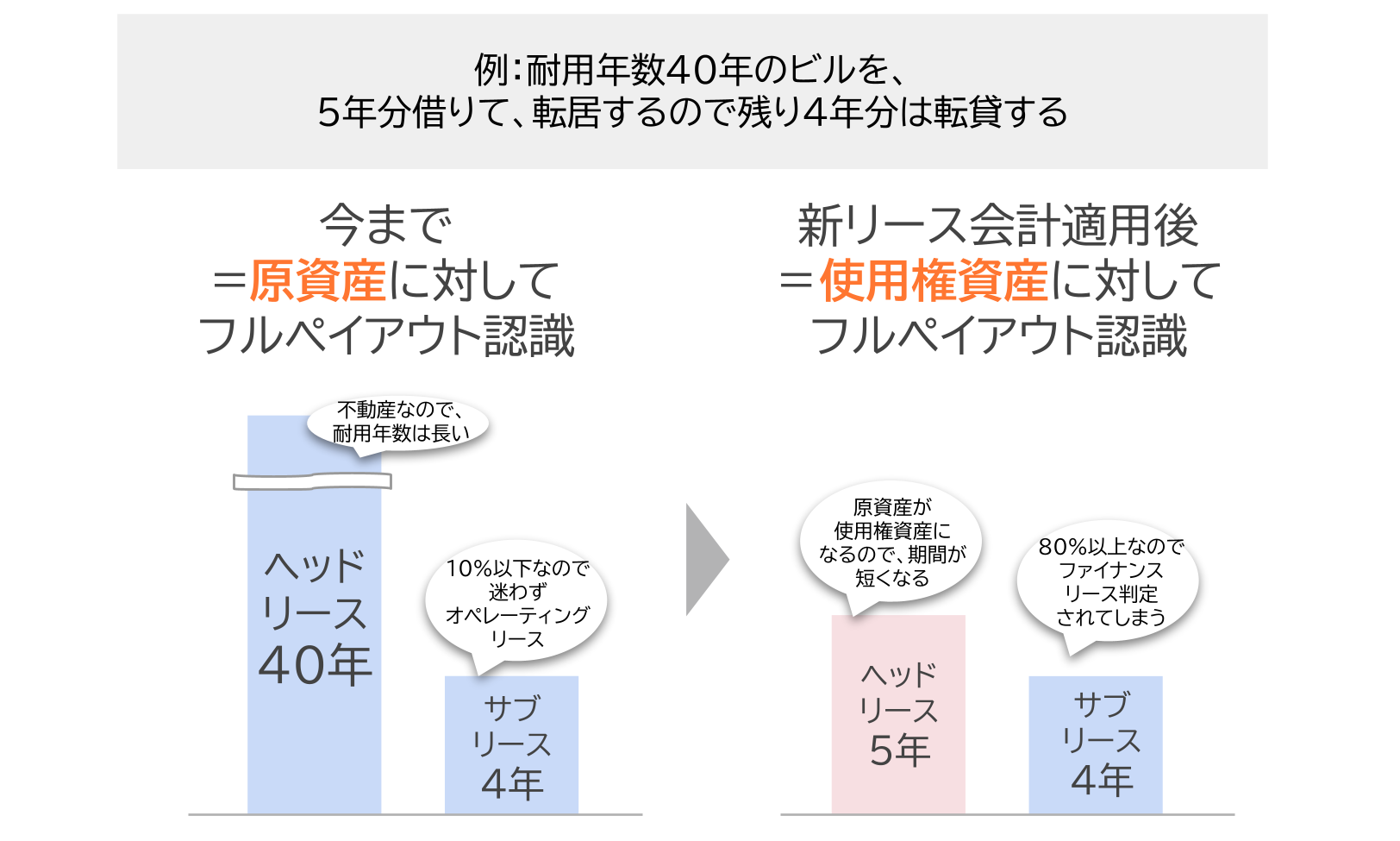

2-3. Subleasing also affects lessor's accounting treatment

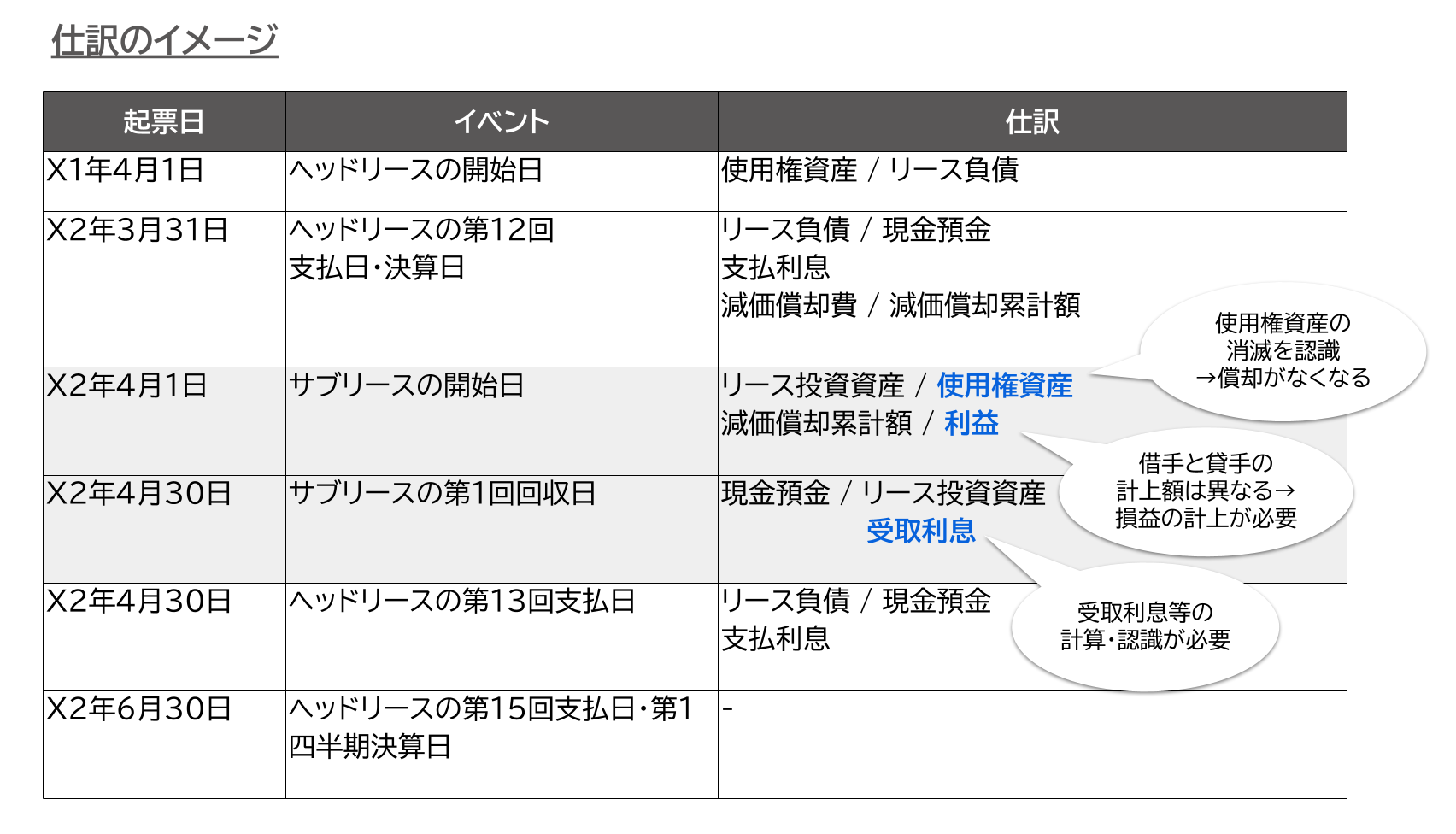

In real estate lease contracts, there are many cases that fall under the category of "sublease," for example, when a property leased by the head office is subleased to a group company. Although the new lease accounting standard has limited impact on the accounting treatment of lessors, it may cause changes in the treatment of "subleases," which is an issue for many companies. Based on the right-of-use asset recognized in the head lease In addition, it is said that the number of cases that must be accounted for using the interest method will increase because the finance lease decision will be based on the right-of-use asset recognized in the head lease.

If the sublease qualifies as a finance lease, Lessee accounting for the head lease and lessor accounting for the sublease should be operated in parallel. At the date of commencement of the sublease, the lessee recognizes the extinguishment of the right-of-use asset and recognizes the difference as a gain (or loss). This results in the elimination of the depreciation base amount on the head lease side, which also affects the amortization calculation. Furthermore, when a termination occurs, the right-of-use asset that has been extinguished must be rerecognized and recognized in profit or loss, which affects not only the treatment of the lessor but also the lessee of the head lease. It is important to design a system that can automatically detect events such as term changes, rent revisions, and terminations of head leases and subleases in the ledger and process them consistently through to remeasurement and journal entries.

3. Summary: Preparing for the increased practical workload caused by the new lease accounting standard

In principle, real estate leases, regardless of the name of the contract, are also subject to on-balance sheet treatment. In considering the actual policy for dealing with this issue, it is inevitable that the final decision will be made for each individual contract.

Therefore, Free generated AI advisory chatbot for on-the-spot review of confusing issues. The following is a brief overview of the real estate lease contract. Based on highly reliable data supervised by a certified public accountant, we provide immediate answers to your practical concerns. We hope you will take advantage of this service.

In addition, whether to use a system or Excel for handling is also an important consideration. Accounting correspondence occurs from the time the contract is signed, and re-measurement during the term increases. In addition, subleases are based on the right-of-use asset recognized in the head lease, which affects not only the lessee's but also the lessor's accounting and increases the workload. Depending on the number and complexity of correspondence, there will be times when Excel will not be able to handle Therefore, we recommend that you consider a policy to deal with this issue, including the introduction of a system.

HUE offers two solutions that can be selected according to the required functions and operations. You can choose the one that best suits your company's situation. Please consider these options.

HUE Asset Product Introduction

Full spec from lessee to contract management and subleasing

New lease accounting compatible system

Read more

HUE Lease Accounting Product Introduction

From 30,000 yen/month, easy and simple to handle

Lessee Lease System

Read more

We hope this article will help you to smoothly comply with the new lease accounting standards.

Supervisor: Mr. Masahiko Inoue (Certified Public Accountant)

As a partner of an audit firm, Mr. Inoue has been involved in auditing and advisory services related to leasing for many years. He is a former leader of the audit firm Tomatsu Lease Credit Industry Leasing Leader and currently serves as a senior fellow in charge of leases at the Accounting Education and Training Organization of Japan in cooperation with the Japanese Institute of Certified Public Accountants (JICPA). He has published a total of eight books on lease accounting taxation in his main publications (most recently, "New Lease Accounting Practical Response and Intuition" published at the end of February 2025). He has served as a training instructor for the Leasing Business Association for many years and has experience as a leasing training instructor in over 30 cases.

\ Seminars related to the new lease accounting standard /

▶ Latest event and seminar information

Related Articles :

Complete Explanation] New Lease Accounting Standards Effective in 2027|Outline, Changes, Impact, and Practical Responses

Three Conditions for Using the ¥3 Million Standard in New Lease Accounting

How to Set the Lease Term under IFRS 16? A Survey of Major Companies in Japan

What journal entries and accounting procedures are required under IFRS 16 (new lease accounting standard)?

New lease accounting standards explained in an easy-to-understand manner! How does it differ from the current standard?

When will the new lease accounting standards become effective? Explanation of the expected timing from the exposure draft!

Related Useful Information

White Paper

2026/02/06

The new lease accounting "business flow" design guide with sample flows.

Web Articles

Jan 30, 2026

How far can you go against the auditors? Real-life battle of new lease accounting and "behind-the-scenes" criteria for system selection revealed by a professional.

Web Articles

2026/01/21

Explanation of the 2026 Tax Reform Proposal for Accounting and Finance - What will change from a practical perspective? What are the changes from a practical perspective?

Related Case Studies

Nankai Electric Railway x WAP talks about the "overwhelming return generated by 'add-on zero ERP'".

Nankai Electric Railway Co.

![]()

Nankai Electric Railway introduces HUE DI and upgrades HUE, Building a Management Foundation that Continues to Adapt to Change

Nankai Electric Railway Co.

![]()

Inventory preparation man-hours drastically reduced. HUE" in a few hours

Huis Ten Bosch Corporation

![]()