Web Articles New lease accounting standard

2020/12/16

New lease accounting standards explained in an easy-to-understand manner! How does it differ from the current standard?

In May 2023, the ASBJ (Accounting Standards Board of Japan) issued an exposure draft of a new lease accounting standard. This standard follows in principle IFRS 16, which has already been initiated by companies that have voluntarily adopted IFRS, and while it will be applied by all Japanese companies, not much is yet known about what actions will be required.

This article provides a basic and easy-to-understand explanation of what the new lease accounting standard is different from the current Japanese standard. (Last updated on December 27, 2023)

Table of Contents

New Lease Accounting Standard Increases Obligations Tenfold?

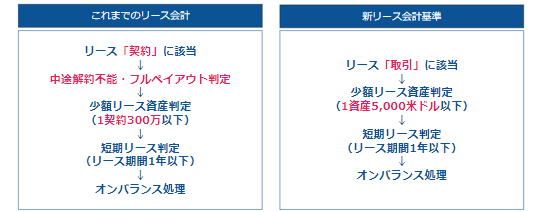

Previous Lease Accounting Standards

Under the current Japanese accounting standards, leases are classified as either "finance leases" or "operating leases," depending on whether they are "non-cancelable" or "full-payout" leases, and if they are not, they are classified as "operating leases. The rules are rather complicated, and finance leases are treated on-balance sheet with exceptions (small amounts or short-term leases).

Definition of Lease in the New Lease Accounting Standard

In contrast, the new lease accounting standard changes the conditions for leases as follows.

- The distinction between operating leases and finance leases is abolished.

- Basically, all leases are accounted for on-balance sheet.

- Exceptions for small value and short term leases will be retained.

(3 million per contract => US$5,000 or less per asset is acceptable)

The exposure draft as of May 2023 is expected to apply this approach directly to Japanese GAAP . In such a case, all real estate leased as business premises and various other contracts will be on-balance sheet, which is expected to have a significant impact on the company's business. It is not uncommon for companies that have already adopted IFRS to see their "liabilities increase by a factor of 10 or more.

Related Article:

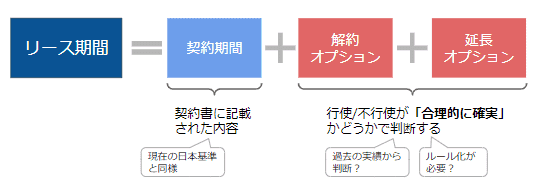

Lease Term ≠ Contract Term? What is the New Contract Term Concept?

Finance leases, which have been accounted for on-balance sheet in the past, were based on the premise that they were "substantially the same as borrowing to purchase an asset," so there were few cases in which the contractual terms changed during the term of the lease.

However, under the new lease accounting standard, leased real estate is also subject to the new lease accounting standard. Therefore, it is not unusual for the terms and conditions of a lease contract to be in flux, such as "a two-year contract is to be extended" or "the rent is to be reduced in the middle of the contract because it is a long-term contract.

Therefore, the new lease accounting standard requires that the lease term is not only the term stated in the contract, but also the " cancellation option (=shorten the term if the contract is likely to be cancelled mid-term)" and " extension option (lengthen the term if the contract is likely to be extended)".

The standard requires that a "reasonable" period of time be estimated based on past experience, etc. However, there are no specific application guidelines in the current IFRS 16, and the reality is that each company determines its own policy in consultation with its audit firm.

Click here for actual application examples: IFRS 16 Application Fact-Finding Survey Report

Is it necessary to adapt your system to the new lease accounting standards?

We have heard from companies that have already adopted the new lease accounting standard on a voluntary basis that their various tasks have increased, such as "journalizing and calculating amortization by on-balancing," "collecting information on contracts from each location," and "managing the amount of impairment of real estate. We also hear that "although we did our best with Excel in the first year, it would be difficult without systemization.

For large companies Fixed asset management system HUE Asset HUE Asset is a fixed asset management system for large companies that supports operations under the new lease accounting standards with standard functions, such as re-estimation of recorded amounts and linkage of lease contract and lease contract data.

Survey of Companies' Actual Responses to IFRS 16 IFRS 16 compliance survey report We are continuously providing information on the trend of legal amendments, such as the "IFRS 16 compliance survey report". If you are interested, please download and review the report.

Related articles:

To request HUE Asset information, please visit

Related Useful Information

Web Articles

Jan 30, 2026

How far can you go against the auditors? Real-life battle of new lease accounting and "behind-the-scenes" criteria for system selection revealed by a professional.

Web Articles

2026/01/21

Explanation of the 2026 Tax Reform Proposal for Accounting and Finance - What will change from a practical perspective? What are the changes from a practical perspective?

Web Articles

2025/11/28

Companies Subject to the New Lease Accounting Standards [Quick Reference] and What Subject Companies Need to Keep in Mind

Related Case Studies

Nankai Electric Railway x WAP talks about the "overwhelming return generated by 'add-on zero ERP'".

Nankai Electric Railway Co.

![]()

Nankai Electric Railway introduces HUE DI and upgrades HUE, Building a Management Foundation that Continues to Adapt to Change

Nankai Electric Railway Co.

![]()

Inventory preparation man-hours drastically reduced. HUE" in a few hours

Huis Ten Bosch Corporation

![]()