Web Articles New lease accounting standard

2021/02/24

What journal entries and accounting procedures are required under IFRS 16 (new lease accounting standard)?

The new lease accounting standard (=IFRS 16) has begun mandatory application for companies that have voluntarily applied IFRS.

It is highly likely that it will be applied to Japanese GAAP in the not-too-distant future, and it is said that it may have a significant impact on the accounting treatment of all Japanese companies as well as IFRS-applied companies.

What specific journal entries and accounting procedures will be required when the new lease accounting standards are applied? In this article, we will explain what journal entries will be required in accordance with actual business scenarios.

Table of Contents

Overview of the changes caused by IFRS 16 (New Lease Accounting Standard)

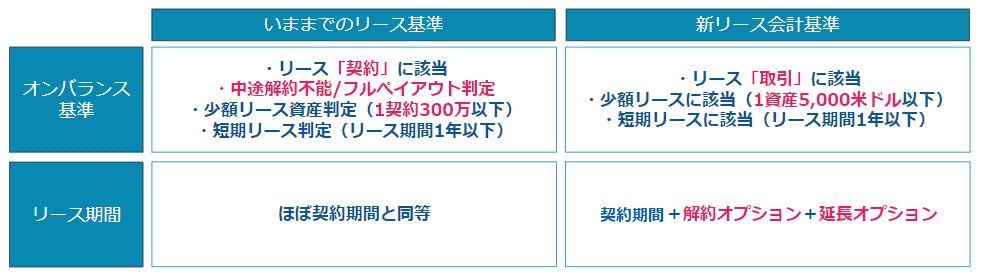

In the new lease accounting standard (= IFRS 16), two fundamental changes have occurred regarding the concept of a lease: "a change in the definition of a lease" and "a change in the concept of the lease term.

First, as for the "change in the definition of a lease," the distinction between operating and finance leases that has been made in the past has been eliminated, and "the right to use something (=right to use)" is now in principle to be accounted for on-balance sheet.

In addition, the standard now clearly states that "the possibility of extending or terminating the lease" should be taken into account, in addition to the term stated in the contract.

Some companies have reported significant effects on their balance sheets, such as a "tenfold increase in the amount of liabilities.

Related articles:

Three journal entries and accounting treatments required by IFRS 16 (New Lease Accounting Standard)

So what will be the impact on accounting practices when the new lease accounting standards are applied? The three main changes that will occur are as follows

(1) Journal entries and amortization and interest journal entries for on-balance sheet treatment

If on-balance sheet treatment is required, the journal entries for capitalization will be required, as well as monthly amortization calculations, interest expense calculations for interest paid, and the posting of journal entries associated with those calculations.

The following chart summarizes the journal entries required for each contract life cycle.

Example: Lease term: 5 years, payment: ³,000,000 (once a month), discount rate: 6%.

Many new journal entries are required for leased real estate, which until now had only to be paid on a case-by-case basis.

Therefore, companies that did not have finance leases before are expected to face a particularly heavy burden.

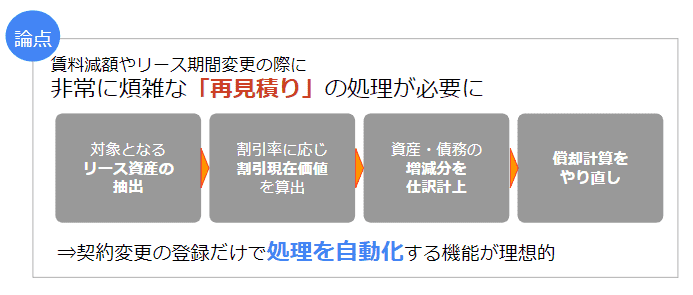

(2) Adjustment of assets and liabilities due to re-estimation

Since real estate is also subject to on-balance sheet accounting under the new lease accounting standard, it is no longer unusual for contract terms and rents to be fluid (e.g., two-year renewal of a contract), and the following "re-estimation" process is required to reflect the results.

In addition to the need to accurately capture information on contract changes, extensions, etc., detailed calculations that take interest into account are required, which can be extremely burdensome.

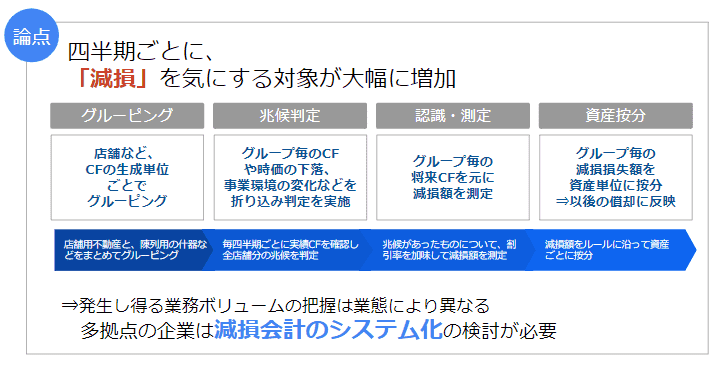

(3) Journal entries for judgmental treatment and book value adjustment for impairment accounting

On-balance sheet contracts are subject to impairment accounting. The impact is particularly noticeable for retail and service businesses that have many stores, as the land and buildings used as stores are also subject to impairment.

The implementation of impairment requires a complex process of grouping, determining the signs of impairment, recognition and measurement, and asset allocation, as described below.

Click here to download the "Latest IFRS 16 Adoption Survey Report for 2021

Is it necessary to adapt your system to the new lease accounting standards?

We have heard from companies that have already adopted the new lease accounting standard on a voluntary basis that their various tasks have increased, such as "journalizing and calculating amortization by on-balancing," "collecting information on contracts from each location," and "managing the amount of impairment of real estate. We also hear that "although we did our best with Excel in the first year, it would be difficult without systemization.

For large companies Fixed asset management system HUE Asset HUE Asset is a fixed asset management system for large companies that supports IFRS 16, including re-estimation of recorded amounts and linkage of lease contract and rental contract data. The new lease accounting standards in Japanese GAAP can also be supported with version upgrades within the fixed maintenance fee.

Survey on the actual status of each company's response to IFRS 16 IFRS 16 compliance survey report We are continuously providing information on the trend of legal amendments, such as the IFRS 16 compliance survey report, etc. If you are interested, please download and review the report.

Related article:

To request HUE Asset information, please visit

Related Useful Information

Web Articles

Jan 30, 2026

How far can you go against the auditors? Real-life battle of new lease accounting and "behind-the-scenes" criteria for system selection revealed by a professional.

Web Articles

2026/01/21

Explanation of the 2026 Tax Reform Proposal for Accounting and Finance - What will change from a practical perspective? What are the changes from a practical perspective?

Web Articles

2025/11/28

Companies Subject to the New Lease Accounting Standards [Quick Reference] and What Subject Companies Need to Keep in Mind

Related Case Studies

Nankai Electric Railway x WAP talks about the "overwhelming return generated by 'add-on zero ERP'".

Nankai Electric Railway Co.

![]()

Nankai Electric Railway introduces HUE DI and upgrades HUE, Building a Management Foundation that Continues to Adapt to Change

Nankai Electric Railway Co.

![]()

Inventory preparation man-hours drastically reduced. HUE" in a few hours

Huis Ten Bosch Corporation

![]()