Web Articles System Review Support

2021/07/29

What is a construction in progress management system? Explanation of functions and benefits that should be confirmed!

For companies in the manufacturing and multi-store categories, the management of "construction in progress," which is the upstream of fixed assets, tends to be complicated. However, because construction in progress management operations vary greatly by industry and business category, unlike the main stream "fixed assets," there are few systems that support it, and in many cases it is difficult to select the right one.

In this article, we will focus on these construction in progress account management tasks and provide the key points and benefits of systemization.

Table of Contents

Three business patterns that should be systemized for construction in progress account management

Although construction in progress accounts can exist in any company, their management can be complicated, and only a limited number of companies require systemization. This section describes three patterns for each type of business.

(1) When a lot of subcontract work is required

One that can occur in many industries is when a large amount of subcontracted construction work is performed. For example, a retailer or service company may subcontract the construction of a new store, a school corporation may construct a school building, or a manufacturing company may subcontract factory equipment. This can be paraphrased as a case where a long-term construction project is required to be recorded as a construction in progress account.

In such a case, the details of the expenses are determined based on "estimates," etc. Therefore, a complicated process is required when transferring the construction in progress account to fixed assets. Since the process of assigning information such as "which itemized amount is an asset and which itemized amount is an expense" based on the details of the quotation (=construction in progress adjustment) is required, there is a high need to streamline the process with a system.

(2) When facilities are constructed by in-house construction

This is the case in the manufacturing industry, for example, where manufacturing facilities are constructed in-house. In this case, the same thing is true for recording long-term construction work as construction in progress, but the process for transferring the information to fixed assets is different.

In the case of in-house construction, detailed information on raw material costs, labor costs, etc. required for construction is often managed in-house. For this reason, it is not necessary to use quotations when performing provisional costing , but rather, calculations are performed from the beginning based on the detailed information stored in the system. Nevertheless, the complexity of the provisional arrangement itself remains the same, so there is a greater need to use the system to perform the process.

(3) When using as a transitional account for purchased goods

The last case is where the construction in progress account is used as a transitional account, although the construction is not particularly long-term. Specifically, the construction in progress account is used in the form of task management, in which all purchased items are temporarily pooled in the construction in progress account, and whether they become fixed assets or expenses is determined and processed by the end of the fiscal year.

In such a case, complex calculations and construction in progress accounting are not usually required. However, since it is necessary to manage the remaining construction in progress in real time in conjunction with other systems, the complexity of Excel and other operations is high, and there are many cases where efficient management by a system is required.

Related page

What is a construction in progress account system? Functions and benefits to check

What points should be kept in mind when considering a system for the construction in progress account, which has various patterns as described above? Here are some points to consider.

(i) Linkage function of expenses from external systems (subcontracting, in-house work, and transitional account)

When managing construction in progress accounts with a system, the ability to link with external systems is also required in many cases. In the case of in-house production, it is necessary to link information on labor costs, raw materials, etc. from internal systems, and in the case of subcontracting or using it as a transitional account, it is also necessary to link order and acceptance inspection information from debt management systems and purchase management systems.

If it is an ERP package, it is necessary to check whether such linkage is possible with the standard functions, and if only the fixed assets and construction in progress area is used, it is also necessary to check the linkage results with external systems.

2) Division and allocation functions (in-house and outsourced)

In the case of in-house work and subcontracting, processing such as "dividing into asset and expense units" based on detailed detailed detailed information and "performing allocation calculations for common construction portions according to the amount" are required.

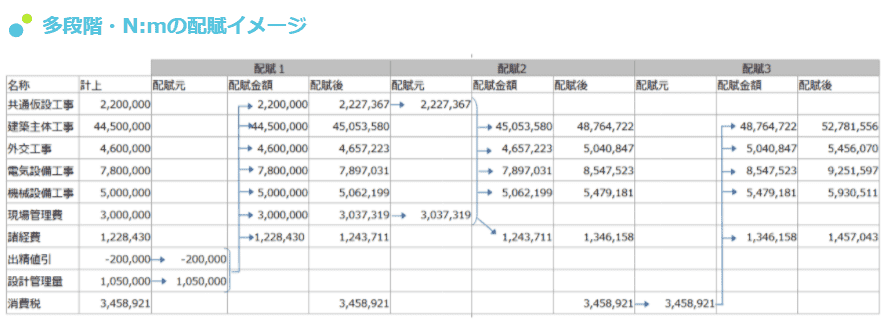

Depending on the requirements, complex calculation processes such asmulti-step allocations andN:m allocations may be required. If these calculations are performed in an "artisanal" manner using Excel, it is important to consider a system function that automates and streamlines the calculations.

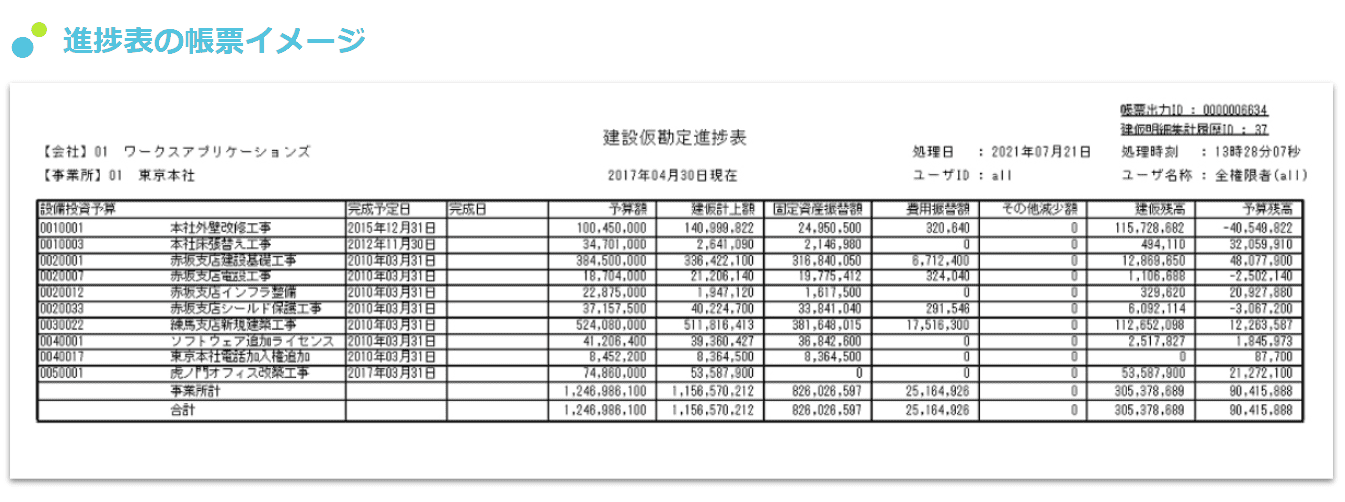

(iii) Inquiry function of progress status

Particularly in the case of manufacturing industries with a long history, construction plans are made based on "capital investment budgets," and there is the task of monitoring and reporting on the progress of the construction based on the construction in progress account.

Therefore, after managing the amount of the capital investment budget, it is necessary to confirm whether there is a function to monitor the progress of the budget by adding up the construction in progress account and the amount of fixed assets transferred from the construction in progress account.

(iv) Function for linking to fixed asset and financial accounting systems

The last thing that is required is the ability to link to fixed assets and financial accounting systems. When a construction in progress account becomes a fixed asset, the system must be able to link that information and prepare journal entries for the transfer, and when it becomes an expense, the system must be able to prepare journal entries for each.

Although many systems are equipped with this function, it is necessary to confirm that it is possible to include even the smallest details, such as whether information on fixed assets is also deleted when a transfer to fixed assets is canceled, or whether a red slip is generated.

Systemization of construction in progress that meets your company's requirements

So far, we have introduced the points that should be checked when systematizing the construction in progress account management. As mentioned in the explanation, the management of construction in progress differs depending on the industry and business category, so it is important to understand the characteristics of your company and select a solution that meets your requirements.

HUE Asset, a fixed asset management system for large companies, covers the level of construction in progress account management functions required by large companies. It flexibly supports inter-system integration, and even complex allocation calculations can be automated and streamlined with standard functions.

Works Applications also continuously provides useful information on system selection, including a collection of fixed asset management case studies that show how asset management operations have been improved at major companies. If you are interested in this information, please download and review it.

Related page:

Related Useful Information

Web Articles

2026/01/21

Explanation of the 2026 Tax Reform Proposal for Accounting and Finance - What will change from a practical perspective? What are the changes from a practical perspective?

Web Articles

2025/11/28

Companies Subject to the New Lease Accounting Standards [Quick Reference] and What Subject Companies Need to Keep in Mind

Web Articles

2025/11/28

New Lease Accounting Standard and Lease Contracts

Related Case Studies

Nankai Electric Railway x WAP talks about the "overwhelming return generated by 'add-on zero ERP'".

Nankai Electric Railway Co.

![]()

Nankai Electric Railway introduces HUE DI and upgrades HUE, Building a Management Foundation that Continues to Adapt to Change

Nankai Electric Railway Co.

![]()

Inventory preparation man-hours drastically reduced. HUE" in a few hours

Huis Ten Bosch Corporation

![]()