Web Articles Invoice System

2020/11/09

What will change in consumption tax calculation with the introduction of the invoice system?

From October 1, 2023, the qualified invoice system (so-called invoice system) will be introduced. The invoice system tends to focus on changes in invoice format, but there will also be changes in the concept of consumption tax calculation, so it is essential to understand the details and prepare a system and operation that can withstand practical use.

This article explains in an easy-to-understand manner what changes the invoice system will bring about in consumption tax calculation and how it will affect business operations and systems.

Table of Contents

What is the invoice system? When does it apply?

The invoice system is a legal revision that "increases the number of items to be included on invoices" and "increases the amount of consumption tax to be paid if an invoice does not include certain items.

Specifically, invoices will be required to include information such as "whether or not each item is subject to the reduced tax rate," "the total amount for each tax rate," and "the number of the business that issued the invoice," and invoices that do not meet these requirements will not be considered "invoices (qualified invoices).

For more information, please click here: [Easy-to-understand explanation] What is the invoice system? What will happen to accounting work?

If you receive an invoice that is not considered an invoice (qualified invoice), the amount of consumption tax you pay will increase.

Related articles:

Will it complicate tax returns? What will change in consumption tax calculation under the invoice system?

So, how will the introduction of the invoice system affect the actual calculation and filing of consumption tax?

The following three major impacts are possible: a significant increase in the complexity of the tax return process, system changes due to changes in calculation methods, and so on.

Changes (1) It will be necessary to determine whether tax credits for purchases are allowed or not.

Under the invoice system, only invoices that fall under the category of "invoice (qualified invoice)" can be used to deduct tax on purchases (*1).

Since only "taxable businesses (businesses that are required to pay consumption tax)" that meet conditions such as "sales of 10 million yen or more in the previous year" are allowed to issue invoices, the accounting department needs to know whether the invoice received is an invoice (= whether the supplier is a taxable business) and change the consumption tax calculation process based on its contents. Therefore, the accounting department needs to know whether the invoice received is an invoice (i.e., whether the supplier is a taxable business) and change the processing of the consumption tax calculation based on that information.

Therefore, it is necessary to implement not only the consumption tax calculation but also the information management of suppliers.

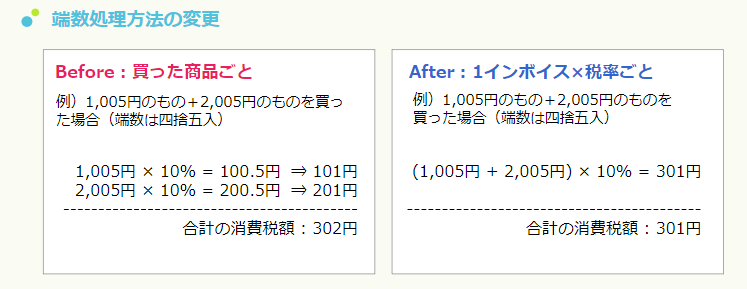

Change 2: Fractional amount of consumption tax is treated "once per invoice, per tax rate".

Before the introduction of the invoice system, the calculation of consumption tax fractions was done for each item purchased.

However, the principle has been changed to "once per invoice, per tax rate" for the fractional calculation under the invoice system.

Example: If you buy 1,005 yen items + 2,005 yen items (rounding off fractions)

This change in calculation method has resulted in a change in the way consumption tax is calculated.

Since such calculations are often performed in payment and receivables/payables management systems, the cost of modifying such systems is expected to be very high.

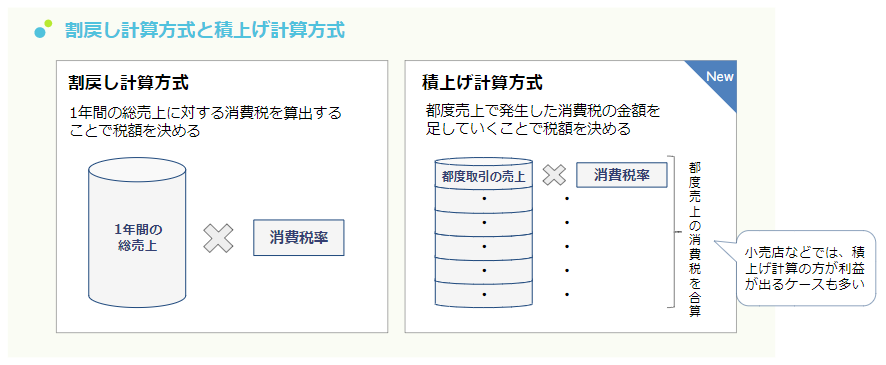

Change (3) "Accumulation calculation" can be used in the calculation of consumption tax amount.

Prior to the introduction of the invoice system, the only method allowed for calculating the amount of consumption tax was the "rebate calculation," which determines the amount of tax by calculating the consumption tax on total sales for the year.

However, the invoice system has made it possible to use the "cumulative calculation" method, which calculates the amount of tax by adding up the amount of consumption tax generated from each sale.

Since there are many cases in which retailers, whose main customers are general consumers, can make more profit by calculating the amount of consumption tax based on the stacked calculation, more companies are expected to adopt the stacked calculation method.

Since the stacking calculation is a calculation method that has not been used before, the time and effort required for the system to support it is expected to be significant.

What systems are needed to cope with the drastically changing invoice system?

Finally, we will discuss the necessity of introducing a system that can respond to the invoice system.

Although we have introduced the changes in consumption tax calculation, the changes are not limited to consumption tax calculation. The changes include the addition of additional items on invoices, additional calculation methods and fractional calculations for consumption tax, and many other things.

In addition to system changes, there are also various trends in the area of invoices, such as electronic invoices, the Electronic Bookkeeping Act, and the paperless system. Since there are many changes in this area, if the system can always respond to these changes, there is no need to spend money on responding to them each time.

The ERP package "HUE" for major companies can respond to changes in laws and systems, including the invoice system, with free version upgrades for a fixed maintenance fee.

In addition, Works Applications is a member of the Digital Invoice Promotion Council, which aims to digitize and improve not only the invoice system but also the business itself, and we can keep up with the latest trends.

If you are interested in our services, we have prepared a useful Brochure explaining the latest trends, which we hope you will download.

Click here to download: A key person of electronic invoicing talks about the latest situation of DX promotion by electronic invoicing.

*The information in this article is based on the laws and regulations as of February 2021. The information in this article is based on the laws and regulations as of February 2021. The contents may be subject to change according to the laws and regulations to be promulgated in the future.

Related articles:

For more information, please contact us at

(*1)

Under the Qualified Preservation of Invoices, etc. method, it is a requirement to keep books and invoices, etc. that contain certain items for the deduction of consumption taxes on purchases.

In addition to the qualified invoices, the following documents are included in the invoices to be preserved (New Act 309).

(a) Qualified simplified invoice

(b) Electromagnetic record pertaining to the matters to be stated in the qualified invoice or qualified simplified invoice

(c) Purchase statement, statement of purchase, or other similar document containing the matters to be stated in the qualified invoice (limited to those confirmed by the counterparty of the taxable purchase). (including electromagnetic records pertaining to the matters to be stated in the documents)

(d) Certain documents (including electromagnetic records pertaining to matters to be stated in the documents) prepared by a person who engages in intermediary or agency business with respect to the following transactions

Sales of fresh food, etc. conducted in wholesale markets as wholesale business under consignment from shippers

・ Sales of agricultural, forestry and fishery products conducted by agricultural cooperatives, fishery cooperatives, forestry cooperatives, etc. under consignment from producers (members, etc.) (limited to those using the unconditional consignment method and the joint calculation method).

The above are the requirements for the amount of taxable purchases. For reasons such as difficulty in receiving invoices, etc., there are other transactions for which tax credits for taxable purchases are allowed only by keeping books containing certain information.

<Reference: National Tax Agency: https://www.nta.go.jp/taxes/shiraberu/zeimokubetsu/shohi/keigenzeiritsu/qa_mokuji.htm#3

Related Useful Information

Web Articles

2026/01/21

Explanation of the 2026 Tax Reform Proposal for Accounting and Finance - What will change from a practical perspective? What are the changes from a practical perspective?

Web Articles

2025/08/01

Behind-the-scenes of the implementation of generative AI functionality in ERP "HUE" for major companies

White Paper

2025/07/24

Introduction to the "Entire Base Establishment Accompaniment Service

Related Case Studies

Paperless and business reform one step at a time! Effects of HUE implementation and future prospects

Yanase Corporation

Reduced 1 million documents per year and realized a paperless office.

Kajima Corporation

Optimizing the entire ERP system with HUE's standard functions by moving away from customization

EXSOL Corporation