Web Articles Invoice System

2020/11/09

What is the invoice system? What will happen to accounting operations?

From October 1, 2023, the qualified invoice storage method (so-called invoice system) will be introduced The introduction of the invoice system is expected to lead to a significant increase in accounting and reporting costs. It is said that the introduction of the invoice system will significantly increase the workload of the accounting department and require system modifications. On the other hand, it is not well known why the invoice system will be introduced and what changes it will bring to business operations. This article provides an easy-to-understand, illustrated explanation of what the invoice system is intended for and how the accounting department and system will be required to respond.

Table of Contents

What is the invoice system? When does it apply?

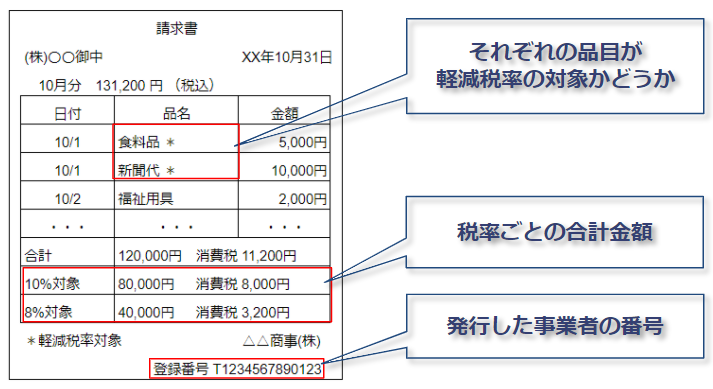

First of all, the invoice system is a legal revision that, from the perspective of the accounting department, "increases the number of items to be included on invoices" and "increases the amount of consumption tax to be paid if the invoice does not include the items.

Increase in the number of items to be included on invoices

Specifically, invoices will be required to state whether or not each item is subject to the reduced tax rate, the total amount for each tax rate, and the number of the business that issued the invoice.

Restrictions on businesses that can issue invoices

The invoice that does not meet these requirements will no longer be considered an "invoice (qualified invoice). If you do business with a non-taxable business and receive an invoice that is not an invoice, the amount of consumption tax you will have to pay will increase.

Therefore, it is necessary to separate the tax treatment for taxable businesses that meet certain requirements (e.g., sales of 10 million yen or more in the previous year) and non-taxable businesses (e.g., tax-exempt businesses including sole proprietors).

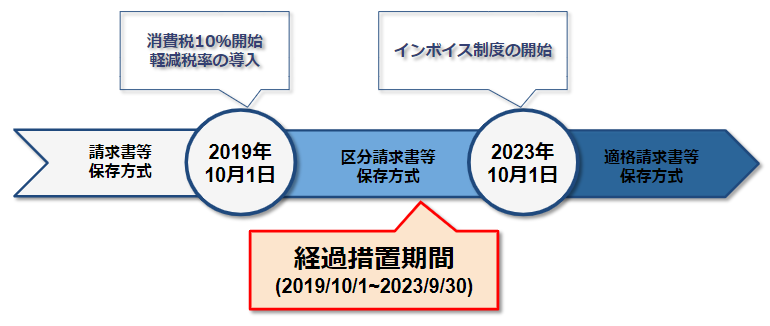

When will the system be applied?

The taxpayers will be required to enter their business number on their invoices, whichwill affect the actual tax amount after October 1, 2023. The transitional measures are scheduled to be fully applied on or after October 1, 2023, when the actual tax amount will be affected and it will also be necessary to include the business number on invoices.

Related articles:

Why is the invoice system necessary? Explanation of the background of the system change

The new invoice system is expected to be in full effect from October 1, 2023. We will explain from the perspective of the implications of invoices and recent trends in consumption tax.

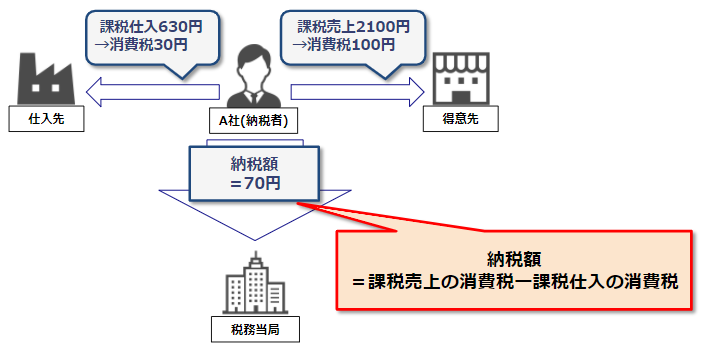

Role of invoices in consumption tax payment

First, we will explain the role that invoices play in the payment of consumption tax. A company is considered a "taxable enterprise" that is required to pay consumption tax if it meets certain conditions, such as having "sales of 10 million yen or more in the previous fiscal year. In this case, the company is required to pay the amount of consumption tax temporarily received from its own customers, but is allowed to deduct the " amount of consumption tax it paid" and pay the tax. (This is called "credit for taxable purchases.

The following is an illustration of how the consumption tax credit works:

In this case, the invoice is used to accurately determine the "amount of consumption tax you paid. Therefore, not only is it necessary to have information on the invoice so that the amount of consumption tax can be accurately ascertained, but it is also legally required to be preserved.

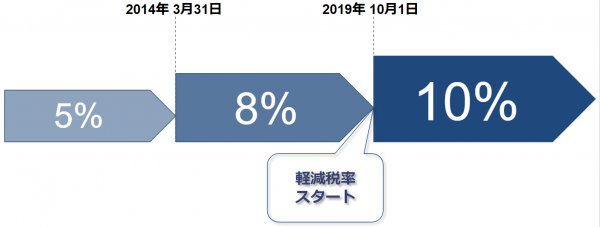

What has changed with the introduction of the reduced tax rate?

Thus, invoices have been necessary for consumption tax reporting for some time, but what triggered the introduction of the invoice system was the increase in the consumption tax rate to 10% in October 2019 and the accompanying introduction of a reduced tax rate.

Before 2019, there was only one consumption tax rate, so the tax amount and tax rate on the invoice The introduction of a reduced consumption tax rate, however, will make it necessary to specify the tax rate and tax amount on invoices. However, with the introduction of the reduced tax rate, there are now multiple consumption tax rates, and it has become necessary for sellers to accurately inform buyers of the consumption tax amount by coloring "which transactions are subject to the reduced tax rate" on the invoice as well. Therefore, the invoice system clearly states "that the item is subject to the reduced tax rate" and "the total amount of consideration for each tax rate" so that the buyer can accurately grasp the amount of consumption tax he/she has paid.

Start of Reduced Tax Rates

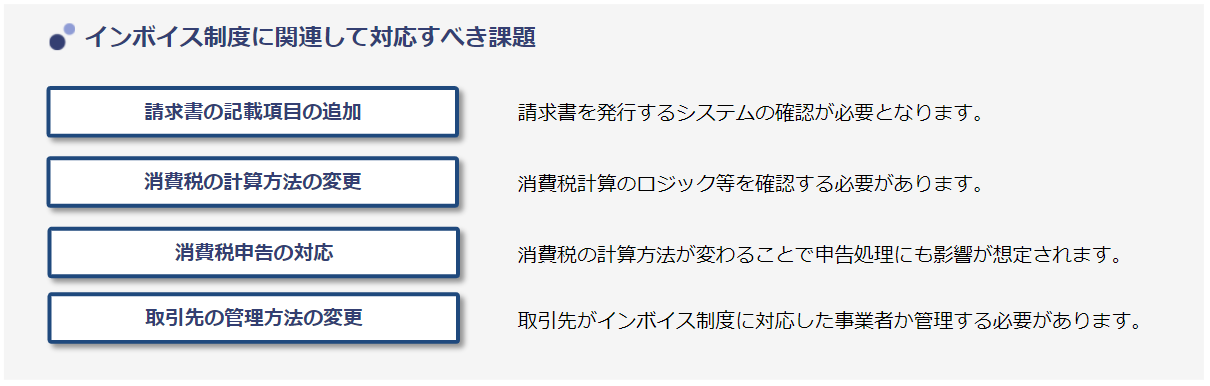

What will change in the accounting department?

So, from a business perspective, what will change as a result of the invoice system? From the perspective of the accounting department of a company, the main effects are that "the format of invoices will need to be changed" and "the work of filing consumption tax returns will become more complicated.

Changes in invoice format

Because there will be more items to be included on the invoice, those who are doing the billing work will need to change the invoice format or change the settings on the system that issues the invoices. Since various items (*2) will be required, system modifications or upgrades will also be necessary if the required items were not originally included.

Complexity of the business of filing consumption tax returns

The invoice system specifies that the tax credit is available only to taxable businesses (in detail, only the tax amount stated on the invoice issued by the taxable business). Therefore, the tax credit for purchases from tax-exempt businesses (including sole proprietorships) and consumers will no longer be available, and the method of calculating the amount of tax will change significantly.

*For more information, please click here:What will change in the calculation of consumption tax with the introduction of the invoice system?

In addition to managing whether a client is a taxable enterprise or not, it will also be necessary to manage each transaction to determine whether the purchase is from a consumer or not.

Click here to download "[5-minute explanation] Introduction to the invoice system - 8 points explained in an easy-to-understand manner

Introducing a system compatible with the invoice system

Lastly, we would like to talk about the necessity of introducing a system that is compatible with the invoice system. The revisions to the invoice system will affect a very wide range of business operations, including invoicing, supplier management, and tax reporting. Since this is an area with a large amount of daily processing, it is essential to have a system that can efficiently handle it in the accounting system.

The "HUE AC" accounting systemsupports legal and system revisions within a fixed maintenance fee. Not only does it support the invoice system, but it also participates in the "Digital Invoice Promotion Council" for the dissemination and promotion of electronic invoicing in the future, enabling it to keep up with the latest trends.

If you are interested, please feel free to Download the Brochure explaining the latest trends.

Related articles:

To request Products / Services, please visit

The information in this article is based on the laws and regulations as of November 9, 2020. The information in this article is based on the laws and regulations as of November 9, 2020, and is subject to change in accordance with the laws and regulations to be promulgated in the future.

(*1)

The "separate invoice" is an invoice in accordance with

, which was adopted as a transitional measure to support separate accounting while maintaining the existing "invoice preservation method". It is scheduled to end on September 30, 2023, and the following items are required to be included.

(1) Name or designation of the issuer

(2) Date of transaction

(3) Details of transaction

(4) Name or designation of the counterparty (recipient)

(5) Indication that the item is subject to reduced tax rates (by adding a "*" mark)

(6) Total amount of consideration (excluding tax or including tax) and applicable tax rate, broken down by tax rate

(7) to (8) are additional items to be included under the invoice system Tax-exempt businesses are also able to issue a "separate itemized invoice".

(*2)

Qualified invoicing business operators are required to include the following items on invoices, etc.

(1) Name or designation of the issuer

(2) Date of the transaction

(3) Details of the transaction

(4) Name or designation of the other party to the transaction (recipient)

(5) Registration number of the qualified invoice issuing business

(6) Indication that the item is subject to reduced tax rates (by adding an "*" mark, etc.)

(7) Total amount of consideration (excluding tax or including tax) and applicable tax rates, broken down by tax rate

(8) Total consumption tax, etc., broken down by tax rate (Total amount of consumption tax, etc. (total amount of consumption tax and local consumption tax))

In the case of certain businesses (businesses that sell to an unspecified number of persons), it is difficult to include the name of the counterparty on each invoice, so a "Qualified Simplified Invoice" can be issued without including the name of the counterparty.

Please refer to the IRS website for more information. National Tax Agency's special site

Related Useful Information

Web Articles

2026/01/21

Explanation of the 2026 Tax Reform Proposal for Accounting and Finance - What will change from a practical perspective? What are the changes from a practical perspective?

Web Articles

2025/08/01

Behind-the-scenes of the implementation of generative AI functionality in ERP "HUE" for major companies

White Paper

2025/07/24

Introduction to the "Entire Base Establishment Accompaniment Service

Related Case Studies

Paperless and business reform one step at a time! Effects of HUE implementation and future prospects

Yanase Corporation

Reduced 1 million documents per year and realized a paperless office.

Kajima Corporation

Optimizing the entire ERP system with HUE's standard functions by moving away from customization

EXSOL Corporation