Web Articles Advanced Business Management

2024/04/30

Trend Words from an Accounting and Finance Perspective Part 2: "Accounting and Finance x Human Capital Management

The areas that accounting and finance departments are required to deal with are expanding year by year, and in addition to traditional day-to-day operations, they are now required to have multifaceted perspectives and information-gathering skills. In this special article, we will focus on a trend word that has been attracting attention as the times change, and will delve into it through an interview with Mr. Sakurada, a senior research committee member of the Japan CFO Association, who is well versed in the accounting and finance area. We hope that this article will provide an opportunity for those in charge of accounting and finance to gain new perspectives and ideas in their daily work. The first trending word is "human capital management.

Table of Contents

Guest: Mr. Shuichi Sakurada

Chief Research Committee Member, Japan CFO Association

Accounting Advisory Inc.

Managing Director/CPA

The era in which non-financial capital creates corporate value has arrived.

The theme of the second session is "Accounting and Finance ✖ Human Capital Management. The "Ito Report on Human Resources ( Note 1) " was the catalyst for the concept of human capital management in Japan, but what is the concept of human capital management in the first place?

The "Ito Report" was published in 2014 as a report of the Ministry of Economy, Trade and Industry project "Competitiveness and Incentives for Sustainable Growth: Building Desirable Relationships between Companies and Investors" chaired by Dr. Kunio Ito. Cost of capital management," which was also the theme of the previous report, is also advocated in this report. However, for many companies, it is difficult to increase corporate value and improve business performance only from a financial and accounting approach. Therefore, the Ito Report on Human Resources was released in 2020 with the recognition that a more essential approach is to focus on "people" and to reform human resource strategies. Human capital management, which is now a hot topic in the economic world, is discussed from the aspect of people as the source of a company's competitiveness.

Professor Shoei Iriyama of Waseda University's Graduate School of Management says that the key to innovation is "the search for knowledge and the deepening of knowledge" as "ambidextrous management. He says that in the world of business administration, it has long been recognized that innovation is born from the combination of existing knowledge. I understand that when many Japanese companies have investigated why it is difficult for new business and DX innovation to occur or why they are lagging behind compared to their counterparts in Europe, the U.S., and China, they have come to the conclusion that they are not allowing their people to play an active role sufficiently.

There is also the issue of shortening business life cycles. Today, there is no guarantee that a business or company will last 40 or 50 years. The economic world has also shown a trend toward job-based employment, as it is difficult to continue a lifetime employment system based on memberships. There is also an active movement among young people to start their own businesses from the beginning. It is also becoming clear that unless reforms are made in the way people work, it will be difficult to attract and retain human resources. In the Corona Disaster, there have been drastic changes, such as the introduction of remote work, which was completely unforeseen in the accounting and finance departments. In such a discontinuous and unpredictable economic and social environment, human capital management is a way to review the state of management from a human perspective.

The "Ito Report on Human Resources" presents three concepts of human capital management in light of the current situation.

The first is to view it in the context of corporate governance reform.

Corporate governance reform is defined as identifying the company's most important management issues, and ensuring that the board of directors and executive officers work together to lead corporate reform under a high-level governance structure at the management level. Human capital management should not be left to the human resource department, but should be implemented by the top management of the company itself. From the perspective of corporate performance, it is on a par with capital cost management. The ultimate goal is to improve corporate performance, which will lead to investment and distribution to the people who make up the company, resulting in greater prosperity for Japan as a whole. This is one policy in that larger context.

Second, we need to discuss this in the context of sustainable enhancement of corporate value. This is an important point. By "sustainable," I am talking about a 10-year span. In the world of business administration, it is said that the determinant of corporate value has shifted from financial capital, tangible assets, to non-financial capital, intangible assets, since around the year 2000. In an era where value is created by intangible assets that cannot be seen, it is precisely people who play a central role, and continuous change over the long term is required, not just being caught up in immediate events.

The third point is that we need the power of the capital markets to bring about change in human resources and human capital. Involving the capital market, rather than merely asking companies to do something as a policy, means considering the revival of the Japanese economy itself with the help of investors, including those from overseas, which naturally requires information disclosure and dialogue with investors. In particular, advanced investors in the U.S. and Europe are strongly interested in human resource strategies.

Direction of Change in Human Resource Strategies Source: Report of the Study Group on Sustainable Corporate Value Enhancement and Human Capital (Ito Report on Human Resource Version)

The "Ito Report for Human Resources" explains the background, the concept of the direction of change, and the approach, etc. The "Ito Report for Human Resources" was released two years later in May 2022. Two years later, in May 2022, the "Ito Report for Human Resources 2.0 (Note 2) " was released. It is a collection of ideas for companies to implement human resources strategies linked to their management strategies. It consists of the following three perspectives and five shared elements. Needless to say, it is necessary to formulate and implement the necessary measures in accordance with the company's management and human resource strategies.

< Three perspectives>

1. Linkage between management strategy and human resource strategy

2 . Quantitative understanding of the as is-to-be gap

Understanding the gap between the business model/management strategy and human resources/human resource strategy

3 . Establishment in corporate culture

Does the implementation of human resource strategy promote transformation of human/organizational behavior and establish it as corporate culture

<Five common elements>

1. Dynamic human resources portfolio

If individuals/organizations/teams are not activated, it will not lead to increased productivity and innovation

2. D&I of knowledge and experience: diversity and inclusion

Diversity of human resources and acceptance of people with different skills, experiences and backgrounds

3. reskilling and relearning

Bridging the skills gap between the desired future and the present

4 . employee engagement

Diverse individuals are proactive and motivated in their work

5 . time- and location-independent work styles

Effective use of remote work, etc.

People are what create value and bring innovation

Starting from the fiscal year ending March 31, 2023, human capital information will be included in the disclosure information for listed companies. Please tell us about the background of this change and how other companies are using the information.

First of all, as I have discussed in the past, the focus should be on "people" in order to sustainably increase corporate value. The original capital that generates corporate value includes both financial and non-financial capital, and since 2000, non-financial capital has been generating more value, and the core of this value is people.

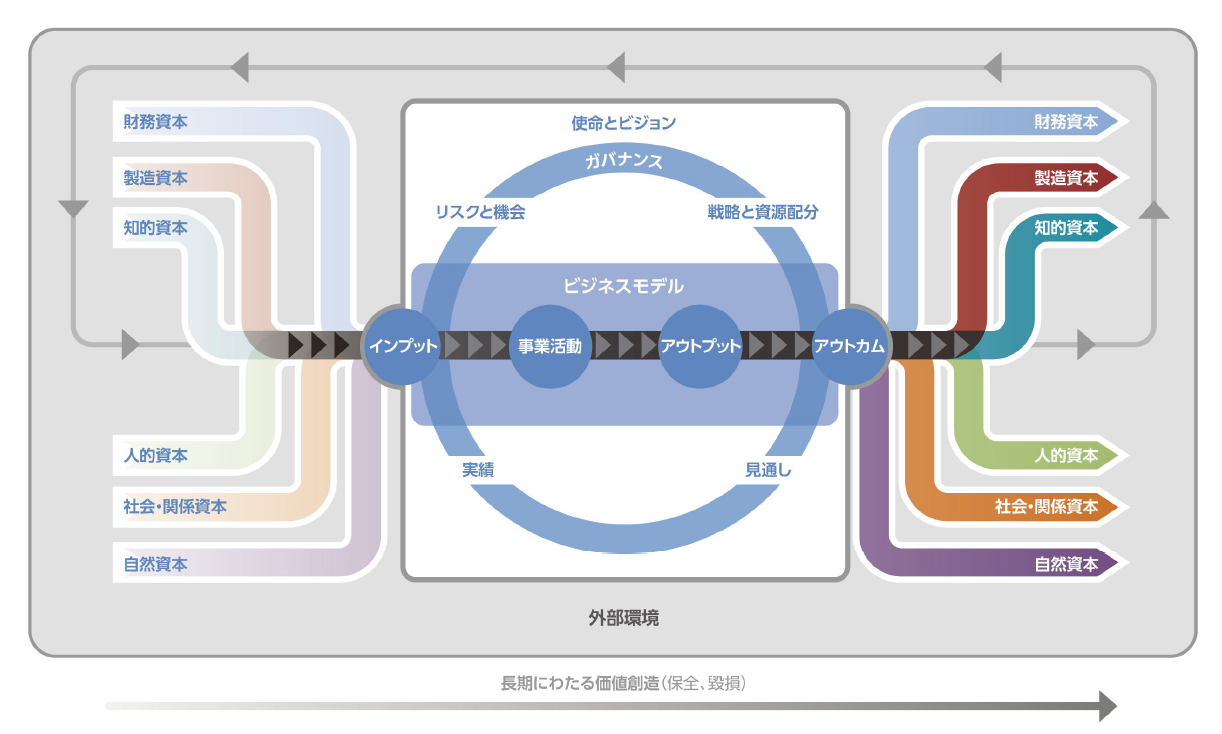

There are various ways of thinking about non-financial capital, but one of the established theories is found in the IFRS Foundation's International Integrated Reporting Framework (Note 3). According to this framework, capital is defined as "the resources and relationships that an organization uses and influences.

Financial capital: financial capital (narrow definition: funds), manufactured capital (assets)

Non-financial capital: intellectual capital, human capital, social and relational capital, natural capital

Depending on who defines it, customer capital and organizational capital may be included, and to some extent the way of definition depends on how management thinks.

Value Creation Process Source: International Integrated Reporting Council (IIRC) International Integrated Reporting Framework

(Value creation is also detailed in Keizai Doyukai: May 2017 "Practicing Capital Efficiency Optimization Management: Value Creation Management through Optimal Use of Financial and Nonfinancial Capital")

Another important point is sustainability or sustainability. There is a growing interest in whether our current society, economy, and natural environment can survive into the future. Investors, especially in Europe, have come to believe that corporate value enhancement cannot be achieved without an emphasis on sustainability. This is so-called ESG investment. And the key elements are non-financial capital, not to mention the central focus on nature, society, and the "people" who make up the companies that influence them.

There are various developments regarding corporate disclosure, but if we focus on the accounting and finance area, in June 2023, the International Sustainability Standards Board (ISSB) of the IFRS Foundation released "IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information" and "IFRS S2 Climate-related Disclosures". The establishment of these disclosure standards by the IFRS Foundation is a very significant move.

In Japan, as is well known, the Tokyo Stock Exchange revised its Corporate Governance Code in June 2021, requiring listed companies to disclose and provide information on investments in human capital and intellectual property. The "Cabinet Office Ordinance on Disclosure of Corporate Information, etc." requires companies to disclose, beginning with their annual reports for the fiscal year ending March 31, 2023, the following information: first, governance and risk management policies and initiatives regarding sustainability in general; second, human resource development policies regarding diversity in human capital, internal environment development policies, the ratio of female managers, the percentage of male employees taking childcare leave, and the percentage of male employees taking childcare leave, The second is the disclosure of human resource development policy regarding human capital diversity, internal environment development policy, ratio of female managers, ratio of male employees taking childcare leave, and wage gap between men and women. In addition, exposure drafts of the Japanese versions of S1 and S2 were released on March 29.

When it comes to sustainability, it is an area that is not limited to the accounting and finance departments. What actions should be taken to begin with in response to the disclosure standards?

Whenever a new standard is released, an exposure draft is issued before the final version. The process is to extract the parts of the exposure draft that are relevant to your company, analyze how they will be affected, and consider what actions will be necessary. Surprisingly, the standards themselves are easier to understand than explanatory books, so the best thing to do is to read the standards. If you have any questions, it would be more efficient to ask questions to the auditing firm or accountant. Once the final version is released, the differences between the exposure draft and the final version will be identified, and if necessary, the differences will be addressed. The final versions of Japanese S1 and S2 are scheduled to be released in 2025 and legally disclosed in 2027.

Regarding the use of information from other companies, it would be good to consider the background and reasons for such disclosures and incorporate what should be incorporated into the company, rather than simply copying what other companies disclose. For example, regarding the adoption of capital efficiency indicators, while consolidated ROE (return on equity) can be calculated, ROIC (return on invested capital), which normally measures the capital efficiency of a business, cannot be calculated without preparing a financial statement for each business segment, even if this is a simplified method. Therefore, ROIC cannot be adopted as a KPI (Note 4) for a business.

Therefore, ROIC cannot be adopted as a business KPI (Note 4). Rather than disclosing ROIC because other companies are disclosing it, it is necessary to properly consider why ROIC as a KPI is necessary, its background, and management strategy.

It is the role of the accounting and finance departments, which are staff organizations, to organize information that can be used as a reference for discussion and consideration by management.

Companies will end if they cannot create opportunities for individuals to play an active role

So far, you have talked about the concept of human capital management from a general perspective. Now, I would like to ask you for your frank opinion.

In the midst of Japan's lost 30 years, a weakening yen, record low labor productivity among OECD countries, and difficulty in raising salaries even in small and medium-sized enterprises, I see the renewed focus on people as a very good thing. However, I strongly feel that we do not want to see human capital management as a superficial, short-term measure. The essence of human capital management should be to increase corporate value, productivity, and profitability.

From a different perspective, given the various discontinuous events that are occurring, it is difficult to guarantee that current businesses and operations will continue indefinitely. This may be a bit extreme, but I believe that there should be a business or corporate model that does not assume permanence.

The idea of lifetime employment is based on the premise of permanence and continuity, but it is no longer a system that necessarily applies to all companies. More fundamentally, I believe that all workers will be required to change, to take on new challenges, to discard old and useless things, and to be open to different knowledge and experiences. In a society where the future is unpredictable, individuals must think carefully about how they will work and live. Companies and managers need to constantly update the framework and systems that continue to provide opportunities for such individuals to play an active role. If this can be done, the company will survive, and if not, it may be the end of the company.

Professor Takashi Iwamoto, a specially-appointed professor at Keio University's Graduate School of Business, spoke at a seminar. Simply put, human capital management is about drawing out the potential of all the people who make up a company and having them play an active role. As a result, corporate value improves and earnings are generated, and I believe that the essence of human capital management is to create such a spiral.

Management evolves through diversification of human resources in accounting and finance departments

Finally, how do you think it is important for accounting and finance departments to be involved in human capital management itself?

The first step is to manage the progress of measures related to human capital management using KPIs. The accounting and finance departments, which are in charge of financial KPIs, the final outcome indicators, should be responsible for the design and operation of the company-wide KPI system. Financial indicators are developed as financial and non-financial targets for each business, organization, and employee, and deviations from actual results are identified, and actions to be taken are determined and implemented. The accounting and finance departments are required to organize the KPI system, develop and operate the system so that it functions as a whole, and importantly, coordinate the linkage between non-financial indicators and financial indicators.

As already practiced by leading companies, quantitative approaches such as multiple regression analysis of the correlation between non-financial indicators and financial statements to determine how KPIs of human capital management and human resource strategy and financial KPIs affect each other are also possible. Even if it is difficult to go that far, we believe that it is necessary to determine what KPIs are needed to realize the management strategy in terms of human resources and how to logically incorporate them into the company-wide KPI system. In doing so, we will be dealing with a variety of non-financial information, including information on human capital, and we will also be responsible for coordinating with many other departments.

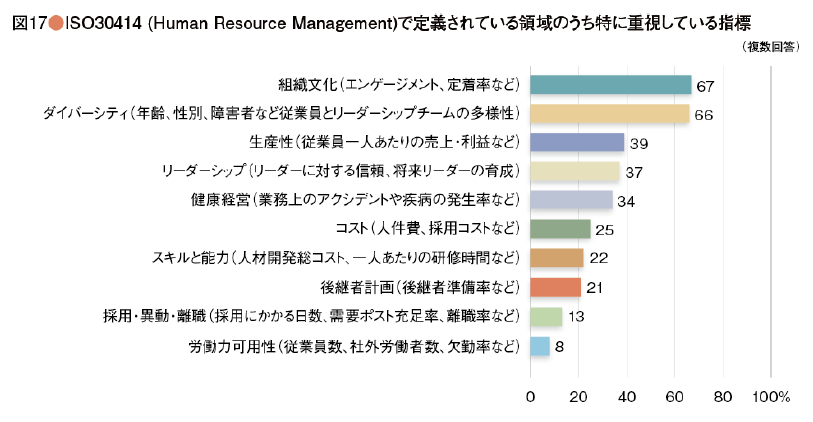

Reference: KPI for human capital management according to ISO 30414 (Note 5)

In addition, the accounting and finance departments, which are ultimately responsible for performance indicators, should take the lead in establishing operational frameworks, such as using IT to collect and process the information necessary for KPIs, establishing and operating a system to visualize this information on a dashboard, and utilizing HR tech applications for KPIs in the human capital area.

Finally, from the perspective of human capital management, the most important aspect of the accounting and finance departments in the future will be diversity and D&I (diversity and inclusion).

By having an organization that is composed of personnel with diverse skills and backgrounds, such as accountants and tax accountants, IT personnel, FP&A experts, and people who used to work in business divisions, not to mention specialists at the level of accountants and tax accountants, the organization will evolve into a stronger accounting/finance organization and become more effective than it is now. I believe that by having an organization that is composed of people with diverse skills and backgrounds, such as IT personnel, people who are strong in FP&A, and people who used to work in business divisions, we can evolve into a stronger accounting and finance organization and support management even more than before.

(Note 1) Ministry of Economy, Trade and Industry: September 2020 "Study Group Report on Sustainable Improvement of Corporate Value and Human Capital - Ito Report for Human Resources -"

(Note 2) Ministry of Economy, Trade and Industry: May 2022 "Study Group Report on Realization of Human Capital Management - Ito Report 2.0 for Human Resources -"

(Note 3) IFRS Foundation: March 2014 "International Japanese Translation of the Integrated Framework", Japanese Institute of Certified Public Accountants, March 2014

(Note 4) KPI (Key Performance Indicator) is translated as a performance management (evaluation) indicator, and is mainly classified into financial outcome indicators and non-financial process (leading) indicators. In recent years, performance indicators are often defined as KGI (Key Goal Indicator) and process indicators as KPI (Key Process Indicator), but it should be noted that KPI is written differently in English.

(Note 5) From Japan CFO Association: March 2022 Financial Management Survey "Strengthening Corporate Governance and Contribution of IT Systems"

The theme of the next "Accounting and Finance ✖ 00 Trend Words from an Accounting and Finance Perspective" will be "Business Automation" and will be distributed around June 2024.

*This article is current as of April 2024

Related Useful Information

Web Articles

2026/01/21

Explanation of the 2026 Tax Reform Proposal for Accounting and Finance - What will change from a practical perspective? What are the changes from a practical perspective?

Web Articles

2025/12/01

Trend Words from an Accounting and Finance Perspective Part 5 (Final)

Accounting and Finance x Dare Now AI "AI Utilization Leads to the Future of Accounting and Finance"

White Paper

2025/11/17

2025 Report on the Status of AI Application in Accounting/Finance Departments

Related Case Studies

Nankai Electric Railway x WAP talks about the "overwhelming return generated by 'add-on zero ERP'".

Nankai Electric Railway Co.

![]()

Nankai Electric Railway introduces HUE DI and upgrades HUE, Building a Management Foundation that Continues to Adapt to Change

Nankai Electric Railway Co.

![]()

Continuously Evolving "HUE" Reduces the Cost of Closing Accounts

Utoku Corporation

![]()