Web Articles Advanced Business Management

2024/03/15

Trend Words from an Accounting and Finance Perspective Part I "Accounting and Finance x Capital Cost Management

The areas that accounting and finance departments are required to deal with are expanding year by year, and in addition to the traditional daily operations, multifaceted perspectives and information gathering skills are now required. In this special article, we will focus on a trend word that is attracting attention as the times change, and will delve into it through an interview with Mr. Sakurada, a senior research committee member of the Japan CFO Association, who is well versed in the accounting and finance area. We hope that this article will provide an opportunity for those in charge of accounting and finance to gain new perspectives and ideas in their daily work. The first trending word is "capital cost management.

Table of Contents

Guest: Mr. Shuichi Sakurada

Chief Research Committee Member, Japan CFO Association

Accounting Advisory Inc.

Managing Director/CPA

PBR Management's awareness required through the demand for PBR

The theme of this first issue is "Accounting and Finance ✖ Cost of Capital Management. In March last year, the Tokyo Stock Exchange requested listed companies to achieve a P/B ratio of at least 1x, and phrases such as " P/B ratio above 1x " and " P/B ratio below 1x " have been attracting attention. Could you first tell us about the background of this trend?

PBR is an abbreviation for " Price Book-Value Ratio," an indicator that shows the ratio of a company's stock price to its net assets. The reason why PBR is attracting attention nowadays dates back to around 2014. At that time, the Japan Revitalization Strategy was announced as an economic policy. Japan's labor productivity is actually low, ranking 30th out of 38 OECD countries in 2023, and its return on equity (ROE) is also much lower than in Europe and the U.S. In short, Japan's labor productivity has been declining for 30 years. Simply put, Japan has not been able to grow for 30 years. As a result, productivity and salaries have not increased. Various measures are proposed and implemented from the perspective of how to revive the Japanese economy. For listed companies, the Ito Report (Note 1), which advocated corporate governance reforms to achieve medium- to long-term sustainable growth and increase corporate value, is an important point of change.

From the logic of the capital market, ROE is the rate of return expected by investors, and from the company's perspective, it is the cost of shareholders' equity. If a company does not achieve a performance that exceeds this level, there is no merit for investors to invest in the company. In the Ito Report, a minimum ROE of 5% is equivalent to the average cost of shareholders' equity in the Japanese market, and if possible, the company should aim for an ROE of8% or higher. Thus, the method of adopting capital efficiency indicators such asROE, ROIC, and ROA that incorporate the concept of cost of capital into performance targets, and deploying them as KPIs for each business, organization, and process to promote management is called cost of capital management.

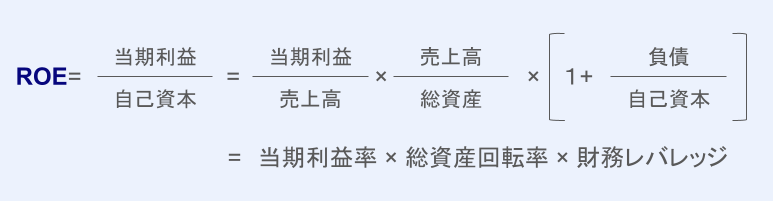

Taking ROE one step further and breaking it down, it is divided into profitability, total asset turnover, and financial leverage (DuPont analysis). In fact, statistical data shows that total asset turnover and financial leverage are not that different from those in Europe and the United States (Note 2). In the end, the most important issue is profitability and productivity.

What is even more important is that cost-of-capital management should not be undertaken from a short-term perspective, but over the medium to long term, from 5 to 10 years. It takes a long time to improve profitability and increase the value of a company's business itself, rather than taking short-term measures.

Unfortunately, even now, nearly 10 years later, the situation of corporate performance has not changed significantly. This is why the Japan Exchange Group became impatient and decided in March of last year to focus on the stock price, which is a straightforward indicator of corporate value, and to aim for a P/B ratio of at least 1x, or in other words, a stock price greater than net assets per share (see Note 3). (Note 3) What is now required of Japanese managers is a change in mindset, a shift away from short-term orientation and conventional business extension, and a shift in direction toward increasing corporate value over the medium to long term.

◆ The biggest management challenge is low profitability

PBR What management issues will emerge in achieving a P/B ratio of more than 1x?

As I mentioned earlier, the biggest management challenge facing most Japanese companies is low profitability. Stock price is an indicator of a company's value in the market, but from a different perspective, it is statistically proven that corporate value is the sum of the present value of future free cash flow. In essence, we cannot expect medium- to long-term growth in corporate value unless we increase current profitability and expectations for future performance. In order to raise expectations for future performance, it is important to communicate information to the outside world and engage in dialogue with investors through IR activities in general. In the end, management itself is being questioned.

Then why are Japanese companies less profitable than their Western counterparts? I believe it is because Japanese companies have not been able to change, and have not been able to transform themselves. As you are all aware, there are issues on the business side, such as the inability to create new businesses, the inability to let go of unprofitable businesses, and the inability of organizations to respond to the shortening of business life cycles, etc. I believe that a major factor is the insufficient use of technology. It goes without saying that the use of technology is an important factor in increasing productivity in the modern era.

In addition, for companies that have already achieved a stable P/B ratio of more than 1x, it is believed that their corporate value can be further enhanced by taking a non-financial capital approach. I would like to discuss this point at another time.

◆ Accounting and finance departments that handle data support the foundation of cost-of-capital management

What role do you think the accounting and finance departments should play in improving P/B ratios?

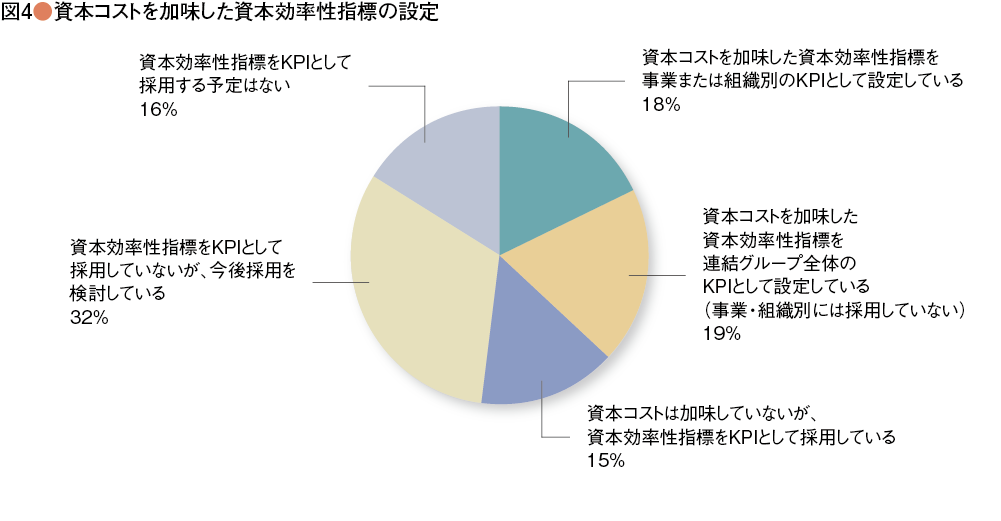

Cost of capital management requires that we make decisions and manage our business based on data. According to the Financial Management Survey "Strengthening Corporate Governance and Contribution of IT Systems" conducted by the Japan CFO Association at the end of 2021, 48% of companies answered that they have not introduced cost of capital management, and that capital efficiency indicators such asROE andROIC based on sufficient data including cost of capital Only 18% of companies answered that they have established cost-of-capital indicators such as ROE and ROIC based on sufficient data, including cost of capital, and that they have properly implemented cost-of-capital management.

Even among those companies that have introduced capital efficiency indicators, a total of 34% have set them only on a consolidated basis and have not expanded them to their businesses or organizations, or have not taken into account the cost of capital.

Of the companies that have introduced capital efficiency indicators, 39% of the respondents answered that they use a simplified method because the accounting systems of their group companies do not allow them to prepare business-by-business financial statements.

Source: CFO Association of Japan, Financial Management Survey, "Strengthening Corporate Governance and the Contribution of IT Systems.

In order to truly utilize capital efficiency indicators, they need to be further developed in a manner that is consistent with the business, organization, and processes, and deployed to target management of front-line operations. Since the accounting and finance department collects all transactional and accounting data, it is responsible for capturing data that makes sense from a business management perspective. If the necessary data is not being collected, the system must be reviewed, improved, and updated together with the information system department, and the management must be educated to understand the need for a long-term perspective. I believe that it is the accounting and finance departments that support the foundation of capital cost management.

◆ Contribute to PBR improvement through active dialogue

What are the key points that accounting and finance departments should be aware of in terms of how they should approach PBR improvement on a practical level?

It is important for the accounting and finance departments to actively engage in dialogue with business divisions and management, rather than being confined to their own roles and processes. This is the so-called business partner function. If there is no role to support business divisions, why is there no such role or organization, or if there is an organization or role but you feel it is not functioning well, what are the needs of business divisions and management? Then, provide business hypotheses and data, and input them. I think it is necessary to create such a cycle.

What impact do you think the introduction and use of advanced technologies will have in improving PBR? How do you think technologies such as big data analytics and AI should be integrated into the decision-making process?

In the case of increasing profitability in order to improve PBR, the use of big data analysis and machine learning has already begun in the area of future forecasting. Big data analysis is used in the retail and other industries.

Big data analysis has been used in the BtoC domain, particularly in the retail industry, but now it is also being used in the BtoB domain to forecast sales and other business performance. It is a statistical approach that performs multiple regression analysis on the relationship between internal and external corporate data, including mainly non-financial data, and performance data such as sales and costs, to establish leading indicators related to performance.

The leading indicators are used to understand the status of goal achievement in each organization and process, to improve on-site activities, and to support decision making. The future PL is created based on the profit structure model created by the accounting and finance departments.

What skills and knowledge do you think are required of accounting and finance department personnel?

It is a good idea to study accounting-related information as a matter of course, and to read information published by the Ministry of Economy, Trade and Industry, the Japan Exchange Group, and auditing firms. Knowledge of finance theory is necessary to understand corporate value and capital efficiency indicators. Together, it is a basic knowledge of corporate management. I think it is important to imagine and understand what managers are thinking, preferably by reading well-established business or management books.

And what I especially want to emphasize is an understanding of data. In this day and age when management is based on data, understanding data is perhaps the most important thing. Without an understanding of the enterprise data model, which data exists in the entire company or group, it is impossible to understand how to collect, maintain, process, and provide the data necessary for management decision-making. In addition, knowledge of statistics for data analysis and forecasting will be essential in the future. It is also important to understand the data flow from the data point of origin to where and how the data is processed, journal entries are made, and ledgers and financial statements are prepared.

In your position and experience in management and business reform consulting, what misconceptions or misguided approaches do you see companies taking to improve PBR?

The most common problem is that capital efficiency indicators such asROE and ROIC are not correlated with the KPIs of each business or organization. This is a case where financial indicators and actual business promotion are disconnected, and the results are simply confirmed at meetings. Capital efficiency indicators must be developed so that each organization, process, and individual can understand what they need to do to improve performance.

Then there is the management timescale I mentioned earlier. Increasing corporate value should be considered over the span of 5 to 10 years, which is the life cycle of an investment or business. I believe that management should focus on the future growth of the company as well as its commitment to annual financial figures. The same applies to the accounting and finance departments that support management. It is important to have a medium- to long-term perspective, with a clear vision and purpose for the direction in which you want to take the company.

(Note 1) Final report of the "Competitiveness and Incentives for Sustainable Growth: Building Desirable Relationships between Companies and Investors" project, Ministry of Economy, Trade and Industry, August 2014

(Note 2) Author's discussion from the first meeting of the study group on substantiating dialogue for sustainable corporate value creation, November 26, 2019, Document 5: Secretariat's explanatory materials

(Note 3) (Note 3) On February 22, 2024, the Nikkei Stock Average reached a new market high while the manuscript was being prepared. This can be seen as a relative assessment of global markets, including the weak yen, the reduction of U.S. interest rates, and the slowdown of the Chinese economy.

The next issue of "Accounting and Finance ✖ 00 Trend Words from an Accounting and Finance Perspective" will focus on "Human Capital Management" and is scheduled to be distributed around April2024.

*This article is current as of February 2024.

Recommended contents for accounting and finance departments

Related Useful Information

Web Articles

2026/01/21

Explanation of the 2026 Tax Reform Proposal for Accounting and Finance - What will change from a practical perspective? What are the changes from a practical perspective?

Web Articles

2025/12/01

Trend Words from an Accounting and Finance Perspective Part 5 (Final)

Accounting and Finance x Dare Now AI "AI Utilization Leads to the Future of Accounting and Finance"

White Paper

2025/11/17

2025 Report on the Status of AI Application in Accounting/Finance Departments

Related Case Studies

Nankai Electric Railway x WAP talks about the "overwhelming return generated by 'add-on zero ERP'".

Nankai Electric Railway Co.

![]()

Nankai Electric Railway introduces HUE DI and upgrades HUE, Building a Management Foundation that Continues to Adapt to Change

Nankai Electric Railway Co.

![]()

Continuously Evolving "HUE" Reduces the Cost of Closing Accounts

Utoku Corporation

![]()