Web Articles Electronic Bookkeeping

2022/02/21 2022/02/18

Revised Electronic Bookkeeping Act Enables Immediate Destruction of Originals?

Under the existing Electronic Bookkeeping Act, even after digitizing receipts and other vouchers, the paper originals must be retained until periodic inspections by a third party, such as a tax accountant, are completed.

The tax reform to be enforced in January 2022 will significantly ease the requirements of the Electronic Bookkeeping Act, including the elimination of the requirement for periodic inspections! . This article will explain whether it is possible to immediately destroy the original documents, referring to the revised requirements.

Table of Contents

Is it possible to immediately destroy paper originals after the revision?

In fact, the timing for the destruction of paper originals after the revision is described in the pamphlet "Tax Reform for FY2021" published by the Ministry of Finance.

In the pamphlet, in the chapter on the revision of the electronic books and records preservation system, it is stated that after the revision, "verification of paper originals will no longer be required (originals can be destroyed immediately after scanning)." It is stated as follows.

Is the immediate destruction of paper originals possible after the revision? The answer to the question, "Can paper originals be destroyed immediately after digitization?

Four requirements that must be met in order to destroy the original documents

In order to destroy the paper originals after digitization, the requirements of the "scanner preservation system" of the Electronic Books and Records Preservation Law must be met.

This chapter explains the four points to be checked in order to meet the revised requirements.

1. Is it possible to digitize paper originals above a certain level specified in the requirements?

When digitizing, the following standards or higher must be met for preservation.

- Resolution of at least 200 dpi

- Red, green, and blue color gradations of at least 256 shades each (24-bit color)

Some services, such as those compliant with the Electronic Bookkeeping Act, provide a function that checks the resolution and other factors when saving electronic data.

In addition, smartphones and digital cameras are allowed to be used for digitization, and the standard of "3.88 megapixels" has been established as an indicator to guarantee image quality equivalent to 200 dpi, so one of the points to check is whether the smartphone or digital camera to be used is compatible. Therefore, one of the points to check is whether the smartphone or digital camera you are using is compatible with this standard or not.

2. Does the system you are using have enough functions to meet the requirements?

There are also requirements that must be met by the system or service that stores the digitized data.

Specifically, the system or service must have functions that meet the following requirements

Requirements for the system or service where the data is stored

✓ Is it possible to record transaction date, transaction amount and counterparty information

✓ Is it possible to download the stored data

✓ If downloading is not possible, can the data be retrieved by specifying a range of dates or amounts?

✓ If downloading is not possible, is it possible to search for data by a combination of two or more arbitrary items

✓ Is it possible to keep a record of corrections and deletions and check them?

It is also important to confirm in advance whether the system or service you plan to use has history management, output, and search functions.

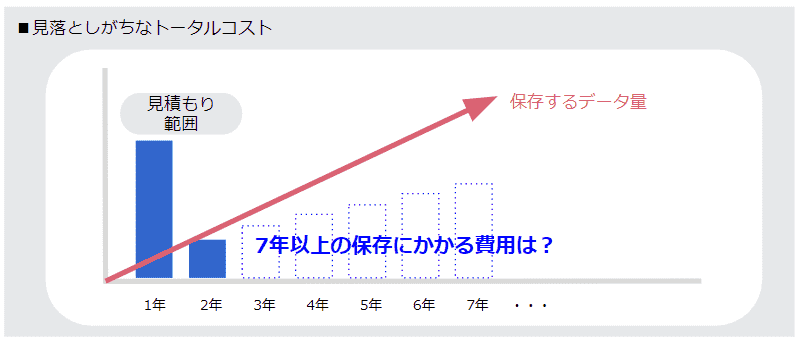

3. Is the system capable of storing data for a period of one year?

The Electronic Bookkeeping Law stipulates that the retention period for digitized data is seven years.

When using a system or service, it is also necessary to confirm that there is sufficient capacity to continue storing the data for seven years.

When requesting a quotation, it is important to assume that the data will be stored for 7 years, so that the actual cost can be estimated.

4. Does the system have measures to prevent tampering and other fraudulent activities?

While the revision has eased the requirements, it has also strengthened the penalties for fraud.

In the event of an omission of declaration, etc., "10%" will be added to the amount of heavy additional tax normally imposed, if it is related to the relevant fraud.

In preparation for the revised taxation system, which requires responsibility for results, including consideration of measures and countermeasures to prevent fraud and omissions, it is necessary to consider measures that can detect and prevent fraud, such as operational or systemic checks.

Related articles:

We can provide a paperless system that complies with the legal requirements.

Many companies are aiming to go paperless by digitizing their paper-based operations, but in order to destroy the paper originals, it is necessary to properly comply with the requirements of the Electronic Bookkeeping Act.

We have also published an article summarizing the requirements of the Electronic Bookkeeping Law and examples of its operation.

In addition, the use of systems and services can be an effective means of detecting and preventing tampering and other illegal activities while meeting the requirements of the law.

At Works Applications, we offer Electronic Book Maintenance, a solution for complying with the Electronic Bookkeeping Law. In addition to history and version management, it is equipped with search functions and other functions necessary to meet the requirements of the law, and has acquired JIIMA certification.

In addition, wecollaborate with a licensed tax accountant who is well versed in the Electronic Bookkeeping Act, and we can also provide consulting services. Please feel free to contact us.

Related Useful Information

Web Articles

2026/01/21

Explanation of the 2026 Tax Reform Proposal for Accounting and Finance - What will change from a practical perspective? What are the changes from a practical perspective?

Web Articles

2025/08/01

Behind-the-scenes of the implementation of generative AI functionality in ERP "HUE" for major companies

White Paper

2025/07/24

Introduction to the "Entire Base Establishment Accompaniment Service

Related Case Studies

Paperless and business reform one step at a time! Effects of HUE implementation and future prospects

Yanase Corporation

Reduced 1 million documents per year and realized a paperless office.

Kajima Corporation

Optimizing the entire ERP system with HUE's standard functions by moving away from customization

EXSOL Corporation